Let’s be honest, most business owners and marketing professionals know that reputation matters. But how many of us can honestly say we know where our organisation rates in how its viewed by stakeholders? Not in a vague, gut-feel kind of way, but with a clear, considered view of the areas that really drive reputation?

That’s exactly why we’ve created RepScale a benchmarking tool which quickly assesses where your organisation sits in terms of its reputation. This free, interactive tool has been designed using decades of experience in PR and communications. It will help you take stock of your brand’s reputational health across five key pillars.

Your reputation is one of your organisation’s most valuable assets, and one of the hardest to rebuild once it’s been damaged. We know from experience that brands which proactively manage their reputation are better placed to attract customers, retain talent, navigate crises and grow with confidence.

Yet reputation is often treated reactively rather than strategically. It becomes something people think about when things go wrong, rather than something that’s nurtured and protected as a core business priority. At Purplefish, we believe that understanding where you are is the essential first step to getting where you want to be.

The scorecard takes you through 20 statements across five reputation pillars — areas we know from working with clients across a wide range of sectors that are fundamental to a strong and resilient brand:

• Media presence & visibility

• Online reputation & search presence

• Crisis preparedness & management

• Thought leadership & authority

• Stakeholder relationships & trust

For each statement, you’ll rate yourself from 1 to 5 — with 1 meaning the area needs immediate attention and 5 meaning you’re excelling with demonstrable results. Your score updates in real-time, giving you an instant snapshot of your reputational health.

At the end of the scorecard, you’ll receive a personalised result with a score out of 100. We recommend aiming for a score of 80 or above, which is our benchmark for a strong, well-rounded reputation. Your result will also include tailored recommendations to help you understand what to focus on next, whether that’s maintaining strength in specific areas or addressing gaps that could be leaving your brand exposed.

It takes around two minutes to complete and it’s completely free. Think of it as a health check for your brand — honest, straightforward and genuinely useful.

Whether you’re a business owner keen to understand your brand’s standing, or a communications or marketing professional looking for a structured way to evaluate your communications strategy, the scorecard will provide quick. Instant insight and clarity to help you plan and manage this fundamental element of any business.

Access RepScale here and if you’d like to talk through your results or explore how a strategic PR approach could help strengthen your reputation, we’d love to hear from you. Book a free consultation with our team and let’s start the conversation.

A deep dive into the UK branding and marketing market from the perspective of independent agencies

(link to full article including interactive heatmap)

Clide Research | February 2026 | getclide.com

When an agency achieves the remarkable feat of 7-digit revenue, the owners (and their teams) are often not content with continuing as a lifestyle business and want to grow further into 8-digit.

A larger agency is not just about more revenue; domain authority does deliver premium pricing (30+%) and better profit margin (5+%).

This is rarely achievable by “doing more of the same”, especially in a market dominated by large global networks at the top. Most agencies try a lot of ideas, which brings the challenge — there are often more ideas than the resources available.

We studied the growth paths of hundreds of UK agencies to analyse what propelled them to 50-100+ people organically, not to offer a playbook, but to illuminate the proven paths and help agency owners anchor their thinking.

The analysis revealed intriguing patterns:

We identified 4 structural changes that independent agencies could seize next 1-3 years, driven by AI adoption and key regulatory changes.

The report concludes with a high-level framework for agency owners to identify the 2-3 strategic bets that best suit them, and how to narrow down to a winning bet.

Getting an agency to seven figures is genuinely hard. Most new agencies never manage it. You survived the project feast-and-famine of the early years, built a team you trust, developed a body of work you are proud of, and found enough clients who value what you do to sustain something real.

The success also means your team no longer just show up to do a job, they gather because of your vision, and what it could mean for their futures. The anticipation for further growth is strong.

You have no shortage of idea. That creative, entrepreneurial instinct is precisely what built the business. It generates hypotheses constantly: a new sector to target, a new service to offer, a new positioning to test, a new market to enter.

The problem is not the ideas. It is the fact that you cannot try everything.

When many ideas are pursued, experiments multiply. The team follows each new direction with diminishing energy. The founding partners become stretched across too many fronts.

This is a familiar pattern at the seven-figure level, and it is not a failure of ambition or effort. It is the natural consequence of a business growing beyond its original design.

Large company chief executives solve this differently. They also face resource constraints and uncertainty, and they invest efforts into identifying a small number of strategic bets that suit their organisations. It’s followed by clear evaluation and aggressive narrow down based on evidence. This approach feels like a luxury when you are building from zero. When you are running a team of twenty or thirty people, it starts to become a necessity.

That is what this article is designed to support. It does not offer simplistic playbooks. It offers a structured view of the UK market from the independent agency perspective, and draws from hundreds of case studies to illuminate the proven paths.

The goal is to help you build conviction from evidence — and then commit to it.

KEY INSIGHT The UK agency fee pool is £8-12bn, but is dominated by large global networks. However, enterprise buyers increasingly prefer best-of-breed capabilities, providing opportunity for well-positioned independents to capitalise.

The UK advertising and marketing market generated £42.6 billion in total spend in 2024, according to the AA/WARC Expenditure Report, and is expected to grow by c.10% per year.

But much of this number is not relevant for independent agencies.

75-80% of this is media spend: the cost of buying airtime, ad space and search/social placement. That money flows through agencies in many cases, but it does not represent fees earned for thinking, creating, or advising. The actual fee pool for branding and marketing services is estimated in the region of £8 to £12 billion.¹

Within this fee pool, the global networks like Omnicom/Interpublic, WPP, Publicis, Havas and Dentsu dominate, by holding the agent-of-record relationships with the largest spenders.

That said, independent agencies have consistently carved out a corner — the top 50 UK independent agencies generated £2.23 billion in the most recent survey year.³ Opportunities usually come from two sources.

Enterprise customers increasingly prefer best-of-breed capabilities on specific areas (e.g. product launches, customer communication, etc.). This opens a wide spectrum to attack for agencies with unique creative philosophy, deep audience understanding or channel expertise.

Most established independent agencies built their businesses in this space and there is a continuous supply of opportunities for up-and-coming agencies. To name a few recent examples:

In each case, the independent agencies provided specialist depth that the networks could not match on that specific brief.

Global networks don’t tend to pitch for customers with <£500k annual fees, constrained by the overhead costs in their business models. This floor is likely increasing due to persistent cost inflation.

This market is collectively large, but the challenge is finding consistent spend streams. The companies in this segment are typically smaller and do not spend consistently on brand strategy and creatives. However, some sectors do reliably spend on communication (e.g. financial services) and downstream marketing services (most B2C sectors).

KEY INSIGHT Financially, scaled agencies are not just bigger versions of smaller agencies. They earn more per person, hold structurally better margins, and have materially more options — including the choice of whether to remain independent.

The 2025 Moore Kingston Smith Annual Survey of UK Marketing Services Companies reveals a clear and consistent gap between group-owned agencies — those within network or PE structures — and independent agencies.

Fee income per head averaged £130,072 at group-owned agencies against £100,926 at independent agencies.³ That is a 29% premium in revenue productivity. At the size where this gap opens up, it is not a marginal difference — it is the difference between a business that generates surplus capital and one that does not.

The margin picture tells a similar story. High-performing agencies — defined as top-quartile for both revenue growth and operating profit — achieved a margin threshold of 18.2%. The industry average operating profit margin was 10.2%.³

These numbers are not benchmarks to aspire toward vaguely. They are a description of what a different business model — one built on specialist positioning, recurring client relationships, and pricing power derived from genuine expertise — actually produces financially.

The mechanism is compounding rather than linear. Specialist positioning commands higher fees. Higher fees fund better hires. Better hires deepen the expertise that justified the premium. Deeper expertise attracts stronger clients, who tend to extend relationships and commission broader scopes of work. Broader scopes generate recurring revenue. Recurring revenue produces more consistent margins.

Each element of that sequence reinforces the next. The agencies that broke through to 100 people did not do so by doing more of what they were already doing. They did so by reaching a position where the compounding effect kicked in — where sector or audience depth was deep enough to justify premium pricing, and premium pricing was sufficient to fund the next hire that deepened the moat further.

KEY INSIGHT Most combinations of sector and specialism could not support an independent agency reaching 100 people. A small number of combinations have consistent examples. The shape of that pattern is not random — it reflects where client spending is large enough, repeatable enough, and specialist enough to support scale.

We studied hundreds of UK agencies and mapped the growth path of 100+ that achieved 50+ people in scale. The analysis focuses on what propelled each agency into scale during its independent phase. Many of these agencies have since been acquired and have expanded into multiple specialisms under network or PE ownership. What matters for this research is the positioning and model that created the foundation — not what the agency became afterwards.

We divided the market into 13 sectors and 11 disciplines. For each growth story, we asked two specific questions:

The heatmap makes the patterns visible. The majority of sector/discipline cross-sections did not consistently produce large agencies. This does not mean opportunities do not exist there — plenty of <50 people agencies built sustainable businesses. It just shows the larger market forces and client spend patterns historically did not support independent scale.

Important: the heatmap does not prescribe a formula. Every growth story has its own ingenuity and market backdrop; it’s too much to cover everything in this report, so we focus on the patterns in the results.

KEY INSIGHT The agencies that scaled all demonstrated strong discipline focus, they occupied positions where the market structure — client budget size, brief repeatability, knowledge barriers to entry — could support a large independent specialist. The breakout opportunities were often presented during significant changes in their target markets.

The heatmap shows five patterns that can be useful for agency owners’ thinking.

The agencies that reached 100 or more people consistently built around a specific positioning — a sector, a channel, a specific audience type, or a defined part of the value chain. Agencies that remained generalist rarely scaled.

This is not a coincidence. Specialist positioning does several things simultaneously: it commands higher fees than generalist alternatives; it creates genuine switching costs as the agency’s knowledge of the client’s world becomes embedded; it builds a reputation within a specific community that makes new business more efficient; and it provides a clear basis for senior hiring. Generalist agencies compete on execution and relationships. Specialist agencies compete on knowledge — and knowledge compounds in ways that execution does not.

FMCG, financial services, technology, and healthcare supported the largest number of scaled agencies. Other sectors attract significant agency activity without producing a meaningful number of agencies reaching 50 people or more.

Property, sports, education, and gaming all show this pattern. Strong creative communities exist. Talented agencies work in these sectors. But no consistent pattern of sizeable independent specialists has emerged.

They share common characteristics: client budgets are smaller or less consistent; brief types lack the volume and repeatability that supports a large team.

The heatmap makes this visible. For anyone considering a deliberate sector bet, this is important information — not a reason to dismiss the opportunity entirely, but a signal that the structural conditions may be working against you.

Looking across the last 3 decades, independent agencies have been consistently fast at capturing, and dedicating to, structural shifts in the broader economy. And such focus is frequently rewarded with scale.

In almost all of these cases, the work they delivered was already covered by existing agencies, but they brought a sharp focus that won the market over. For example:

With the exception of performance marketing, we found no visible examples of an independent UK agency reaching 100 people by focusing primarily on mid-market clients. Even startup-focused Koto has since expanded into digital-rebranding for enterprise customers.

This is a meaningful finding, because the mid-market is where many independent agencies get their early new business. Mid-market clients have smaller budgets, typically want a broader range of services than a specialist can efficiently provide, and tend to be more price-sensitive.

The agencies that scaled worked with large companies — often ones where global networks were also present on different parts of the account. The independent won a specific mandate, not the whole relationship. The brief was large enough to justify the expertise, and the client was sophisticated enough to value it.

This does not mean mid-market clients have no role. They are often where the specialism is first developed and proven. But scaling required moving up the client tier, not across it.

Brand strategy is a frequently used phrase to encapsulate the work by an agency. Intriguingly, very few agencies have reached scale by focusing on brand strategy/architecture alone (with limited/no creative), almost none in recent years.

This reflects the traditional high value segment for brand strategy (brand transformation, mergers & acquisitions driven brand consolidation, major rebrand) is increasingly taken by large global networks; yet the brand strategy spend by smaller companies is not sufficient to support an agency at scale.

There are smart angles such as Brand Finance turning brand valuation into a product (WPP has similar capabilities, but used more internally), but that’s more an exception than a pattern.

KEY INSIGHT The agencies that scaled built positions where the pricing power lived in their thinking, not their production. All three growth architectures involve execution capability — but in each case, the execution is the delivery mechanism for specialist knowledge, not the source of the value.

Across the agencies that exceeded 50 or more people independently, three distinct growth architectures emerge.

The growth paths across the architectures are similar. Deep knowledge commands premium fees. Premium fees fund specialist hiring. Specialist hiring deepens the moat. A deepened moat attracts international clients — and international clients create the natural demand for a second studio, which is typically the inflection point that changes the growth trajectory from linear to compounding.

These agencies consistently sold downstream into implementation as they scaled — packaging production, communications delivery, campaign execution — creating significant revenue volume on top of the strategic and creative fees. But their downstream offering is focused on their specialty, avoiding significant ballooning of headcount usually associated with downstream services.

An agency that builds institutional knowledge in a specific industry sector, and tangibly tailors how it approaches its specialist discipline — the clients regard it not as experienced, but as genuinely expert. The moat is the knowledge and demonstrable approach, perpetuated by a growing roster of highly relevant case studies.

The knowledge starts to live in the agency’s processes, methodologies, and people — not just in the founder. That is what makes it scalable.

This architecture is most commonly observed in creative and communications specialisms. Creative specialists focused on FMCG and consumer brands produced the most successes, for example:

Financial services communication specialists produced the second largest cohort of scaled agencies, for example:

Technology corporate communications specialists produced the third largest cluster, for example:

Healthcare and pharmaceutical is also worth a mention, supporting multiple communications specialists to above 50 people (e.g. Madano, Hanover Communications, etc.) and helped Lynx grow to 400 people.

Deeply expert in a specific audience type: consumers, investors, employees, a particular demographic or cultural community. Many scaled agencies focused further on an audience type within a sector (e.g. financial services shareholders).

The moat is built on audience insight and a methodology that’s visibly tailored for the audience. The positioning is: we know how to speak to this audience — and that understanding is proprietary, systematic, and often transferable across client sectors.

Some notable examples:

The audience-focused model is one of the most dynamic over time, heavily driven by the way people consume information and generational shift.

The sophistication of search and social channels increased in line with the rising usage by advertisers; extracting optimal performance started to require deeper channel-specific expertise.

Unlike traditional media buying, the concentration of the channels created large execution-focused agencies. It’s also one of the rare examples where mid-market clients provided growth engines given their significant and consistent performance marketing spend.

The winners are focused on data but also have knowledge about content-channel fit and deploy proprietary software to link campaign management data to the client’s systems. They usually work alongside creative firms, delivering content rather than creating it.

Scaled agencies in this model usually have high headcount (large offshore workforce to handle manual processes), some examples:

KEY INSIGHT The agencies that scaled most dramatically did not do so only through internal excellence. Their growth was typically punctuated by structural market changes that created demand for specific capabilities at the right moment. Multiple structural changes are unfolding in the UK in the next 1-2 years.

As we discussed in Section 4, seizing structural changes in the market has created a large number of scaled agencies.

Looking further back in history, this pattern holds extremely well. FMCG packaging specialists scaled on the back of globalisation. As brands expanded from domestic markets to international portfolio management in the 1990s and 2000s, the agencies that had built the deepest expertise in brand design and packaging found that the same global clients who valued their work in the UK needed it replicated in Amsterdam, New York, and Singapore. The agencies that followed their clients into new markets grew significantly larger than those that did not.

Healthcare communications specialists scaled on pharmaceutical deregulation and the global clinical trial boom of the same era. Corporate communications agencies scaled on the privatisation waves of the 1980s and 1990s, and more recently on the rise of ESG disclosure requirements that created volume demand for stakeholder and investor communications.

In each case, a structural shift in the market created conditions where a specific type of specialist expertise became substantially more valuable. Agencies already positioned in that space captured a disproportionate share of the resulting demand.

Structural changes in the UK to watch out for

Several structural changes are afoot in the UK at the moment. Below are a few that are unfolding in real time and could have systematic impacts on how companies approach branding and marketing.

UK HFSS restrictions on advertising of high-fat, salt, and sugar products — which came into force on 5 January 2026 for TV and online channels — are creating a material change in where major food and drink brands allocate their marketing budgets.¹⁴

A few reaction patterns are emerging:

Industries experiencing rapid AI-driven disruption — software, professional services, financial services, education — are under significant pressure to articulate their value proposition in a world where their investors expect their core offering to be impacted by AI. The brands that navigate this well need genuine strategic depth: the ability to reframe positioning, rebuild messaging architecture, and communicate clearly through a period of structural uncertainty.

This creates demand for strong communication capabilities and the ability to deal with the urgency of the situation (a broad spectrum of companies have suffered 20+% share price decline in the first two months of 2026). The window in which a brand can define its position in an AI-disrupted landscape is not indefinite — the categories are moving fast, and early positioning decisions will be difficult to revise.

AI chatbots have taken a visible chunk out of search activities, and the trend is likely to increase with the chatbot builders rapidly rolling out new use cases (e.g. shopping, travel planning, etc.).

This changes the way consumers access information, which will likely impact how brands communicate with them effectively:

Marketing and customer services are the first two areas that saw mass AI adoption. While this brings efficiency and gives customers a faster experience, the de-personalisation and the repetitive “AI tone” are also drawing customer resentment.

As AI adoption grows further, brands will most likely start to respond and seek to bring on-brand tones and communication approaches to their AI agents.

Multiple startups recently backed by Y Combinator are already focusing on delivering on-brand and personalised experiences via AI agent, indicating growing awareness of the issue. And Definition already lists a service that helps to tune their client’s AI agent.

KEY INSIGHT Most agency founders know what they believe they are best at, but market forces and competition could mean the commercial results look different. A commercially honest audit is the crucial foundation for strategic planning.

The market map and the three growth architectures are useful frames. But the actual paths have to be built from your own data. You have intuition about what you are good at, but that should be checked against what your business has won, charged and retained, and profited to clarify your genuine competitive advantages.

A structured way to surface that signal is to review the last three years of work through four lenses simultaneously.

Fee rates and margins by sector and service type. Where has pricing been strongest? Where have write-offs been lowest? The data almost always reveals concentrations the team has not consciously registered. If you have consistently charged more for a specific type of brief than any other, that is worth understanding.

Client lifetime value by segment. Which engagements led to extended relationships, expanded scopes, and referrals? Long-tenure clients are not just commercially valuable — they are evidence that the agency is delivering something the client cannot easily replace.

Close rate by brief type. Where does the agency win most consistently? High close rates in a specific category are a reliable signal of genuine competitive advantage. Low close rates in a category you are actively pursuing is a signal worth paying attention to.

Team energy. Which types of work generate genuine engagement from your best people? The alignment between what the team finds meaningful and what the market rewards well is the foundation of a durable position. Misalignment — strong commercial performance in areas the team finds draining — is a warning sign for sustainability.

The intersection of all four is where your positioning should be built. In most agencies at the seven-figure level, this intersection is considerably more specific than the agency’s current official positioning suggests.

Once you have identified your strongest intersection through the commercial audit, the next question is which paths you should bet on.

You are usually the main salesforce, and your time is limited, so it’s critical to identify 2-3 strategic bets that exemplify your strengths.

Home in on your star discipline, identify 1-2 sectors where you and your team feel strongly, and that have sufficient spend power. Create positioning ideas with your team that captures potential catalysts facing those sectors that you can address better than anyone else. This makes sure everyone is on the same page and attacks these angles at full energy.

No plan survives contact with the enemy. Adjustments will be necessary. That’s why it’s critical to have full visibility on progress in real time. When you feel the need to try a new angle, it means at least one of the existing angles should be shut down. This is critical to ensure you do not overstretch your resources and your own bandwidth.

Moat first. Scale follows.

1. AA/WARC Expenditure Report, April 2025 — UK total advertising expenditure £42.6 billion in 2024. Media spend proportion estimated by the authors. https://adassoc.org.uk/our-work/uk-advertising-records-42-6bn-spend-in-2024/

2. Omnicom Group and Interpublic Group merger announcement, December 2024; merger completed November 2025. Combined revenue figures per company disclosures. https://investors.interpublic.com/news-releases/news-release-details/omnicom-acquire-interpublic-group-create-premier-marketing-and

3. Moore Kingston Smith Annual Survey of UK Marketing Services Companies, 2025. https://mooreks.co.uk/insights/snapshot-annual-survey-on-the-financial-performance-of-marketing-services-companies-2025/

4. Historical analysis of Publicis/Saatchi and WPP/JWT merger periods; authors’ assessment.

5. Epoch Design company profile; client claims per company website. Employee count per 6sense and LinkedIn data, February 2026. https://epochdesign.com/

6. PMLiVE — Havas Lynx company profile and Campaign Healthcare Agency of the Year citations. https://pmlive.com/pmhub/havas_lynx/

7. Dentsu Aegis Network — Gyro International acquisition announcement, July 2016. https://www.dentsu.com/us/en/news-releases/dentsu-aegis-network-acquires-gyro

8. Emperor Design — company website and Companies House filings. https://emperor.works/about/ | https://find-and-update.company-information.service.gov.uk/company/03160710

9. Buttermilk — company website and Favikon employee data, February 2026; Unilever appointment per industry press, 2025. https://thinkbuttermilk.com/

10. Amplify — Brand Experience Agency of the Year 2024; financial figures per company announcement. https://weareamplify.com/

11. The Imagination Group Limited — Companies House filing, August 2024 accounts. https://find-and-update.company-information.service.gov.uk/company/02275977

12. Inflexion Private Equity — Goat Agency investment announcement, March 2021; WPP — Goat Agency acquisition by GroupM, March 2023. https://www.inflexion.com/portfolio/goat/

13. Brainlabs, Croud, and Jellyfish — company profiles and PE/acquisition announcements per company and investor disclosures. https://www.brainlabsdigital.com/ | https://www.croud.com/ | https://www.jellyfish.com/

14. ASA/CAP — HFSS advertising restrictions on less healthy food and drink, came into force 5 January 2026. https://www.asa.org.uk/news/new-rules-and-guidance-for-less-healthy-food-and-drink-advertising.html

Clide helps independent branding and marketing agency owners think through the strategic questions that will shape the next five years of their business.

getclide.com | © Clide 2026

Average Agency Salary in the South West: Digital Marketing Salary Guide 2026.

This article first appeared on the ADLIB Blog.

How we benchmark salaries and rates

What to consider when assigning a salary

Comprehensive salary guide for agency roles in the South West

Bulletproof – The Event Every Agency Owner Can’t Afford to Miss

2026 marks the third post-COVID edition of the Bulletproof Agency Network conference, and this year, we’re raising the bar.

We’re heading back to the stylish surroundings of VOCO Manchester for a day designed to challenge your thinking, sharpen your strategy, and reconnect you with what makes agency life exciting in the first place. Expect bigger conversations, deeper insights, and more meaningful connections than ever before.

The theme for 2026 is “Pitch to Partnership.”

Because winning work is only the beginning. The agencies that truly thrive are the ones that know how to turn a single opportunity into a long-term, high-value relationship. This year is about mastering that transition – from proposal to partnership, from project to profit, from client to collaborator.

Let’s be honest: running an agency can feel relentless.

You’re balancing delivery and growth. Managing people and expectations. Navigating uncertainty while trying to stay commercially sharp and creatively relevant.

Bulletproof exists for that reality.

Imagine spending a day surrounded by people who genuinely understand the pressures you’re facing, leaders who’ve made the mistakes, solved the problems, and discovered what actually works. Not theory. Not fluff. Real-world strategies, honest conversations, and practical ideas you can take back and apply immediately.

That’s the difference.

Bulletproof isn’t just another conference.

It’s a reset button for ambitious agency owners who want more. More clarity, more confidence, and more control over where their business is heading next.

Meet this year’s lineup of industry experts

This year’s conference features an outstanding lineup of speakers who’ve mastered the art of scaling businesses, leading teams, thriving through challenges and building resilient agencies.

Keynote speakers include:

Trenton Moss

Founder of Team Sterka, he puts his agency’s success down to one thing, making everyone a leader.

Katie Bolas

Ex-agency leader turned Fractional Operations Director, who helps agencies succeed by fixing the operational issues that drain profit and frustrate teams.

Claire Richardson-Critcher & Steve Byrne

Co-Founders of As The Crow Flies, they are renowned for their ability to cultivate powerful, sticky habits that create proper confidence when forecasting New Business.

Hosting the event is Dan Archer of Suprpwr Consulting, he’s all about helping businesses make marketing their Superpower.

And it’s not just the keynote talks. Attendees will dive into specialist-led sessions packed with legal, financial and insurance insights designed for the unique challenges of creative and digital agencies.

Experts such as Steve Kuncewicz (Glaisyers), Paul Barnes (MAP) and Michael Henderson (Riskbox) will be sharing their insights to help future-proof your agency.

Bulletproof isn’t just a conference, it’s a community.

This isn’t just a day of learning, it’s your chance to meet other agency owners who truly get what you do, swap stories, celebrate wins and lessons and walk away with connections that last long after the conference ends.

Grow Your Agency, Support Your Community

Bulletproof 2026 isn’t just about learning and growing your agency, it’s about making a real impact while you do it. 100% of ticket proceeds will be donated to 2 incredible local charities: Forever Manchester & Barnabus , so you can level up your agency while giving back to the community.

Join the Leaders Shaping the Agency World

After last year’s amazing day, demand is already high for Bulletproof 2026, so don’t miss your chance to be part of a day that will leave you inspired, connected and ready to take your agency to the next level.

Grab your ticket here & join us on the 7th May for an unforgettable day.

The creative industries contributed £145.8bn in gross value added (GVA) to the UK economy in 2024, new government figures have revealed.

Creative industries GVA rose by 4.6% between 2023 and 2024, compared to the UK economy as a whole which grew by 1.0%, the data from the Department for Culture, Media Sport (DCMS) shows.

The sector’s GVA was 19.7% higher than pre-pandemic (2019) and 60.3% higher than in 2010, in real terms.

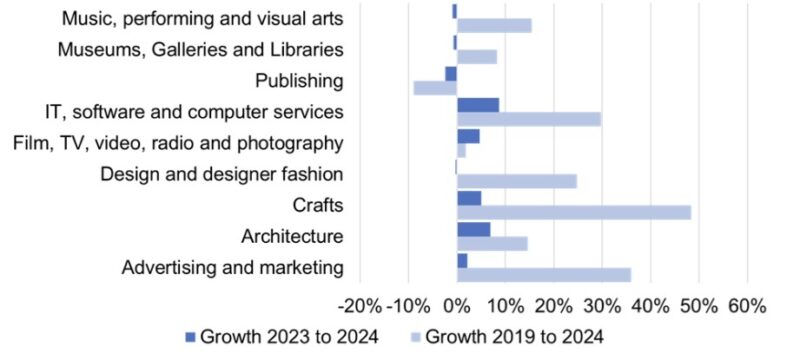

The growth was driven by the ‘IT, software and computer services’ subsector which increased by an estimated 8.7%, followed by ‘film, TV, radio and photography’ and ‘advertising and marketing‘ which grew by 4.6% and 2.1% respectively.

‘IT, software and computer services’ is the largest subsector of the creative industries by GVA, contributing an estimated £62.4bn in 2024. ‘Advertising and marketing’ is the next largest with £24.3bn.

Growth in creative industries subsectors, in chained volume measures (CVM):

Other data released this month showed the creative industries account for almost a 10th of UK firms classified as having ‘high-growth potential’, and a lot of those businesses are in Bristol and the south west.

The DCMS report also included data for the cultural sector which contributed an estimated £40.3bn in 2024, accounting for 1.5% of UK GVA.

GVA grew by around 2.4% from 2023 to 2024, compared to the UK economy as a whole which grew by 1.0%. From 2010 to 2024, culture GVA grew slightly faster than the UK economy (25.4% vs 24.3%).

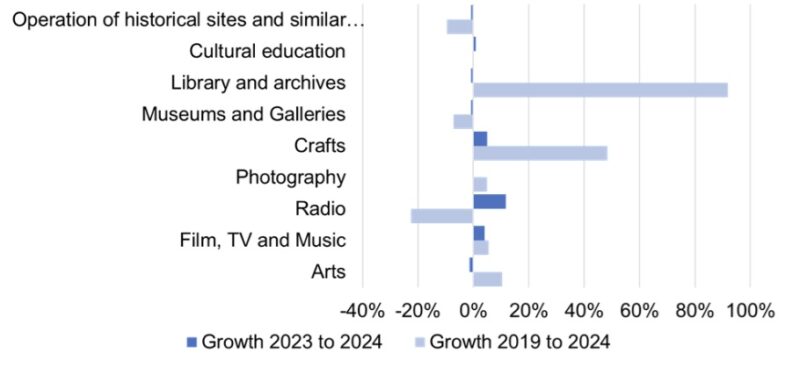

DCMS said the increase in cultural sector GVA was almost entirely due to a 4.1% increase in the ‘film, TV and music’ subsector.

The subsectors that saw the largest relative growth in cultural sector GVA were the ‘radio’ which increased by an estimated 11.8% and ‘crafts’ subsector which grew by an estimated 4.9%.

‘Film, TV and music’ is the largest cultural subsector in size economically, contributing an estimated £23.8bn to the UK economy in 2024. The second largest is ‘arts’ with £11.4bn.

Growth in cultural sector subsectors, in chained volume measures (CVM):

Alongside the data for the growth of the creative industries, the government has announced new funding and related support for creative businesses.

It follows the publication last year of the creative industries sector plan. In addition, the creative industries is one of the eight key sectors of focus in the government’s industrial strategy and the West of England is one of the government’s priority areas for the creative industries. As part of that, the £25m Creative Places Growth Fund will run for three years from April 2026.

The new funding and support announced this month is:

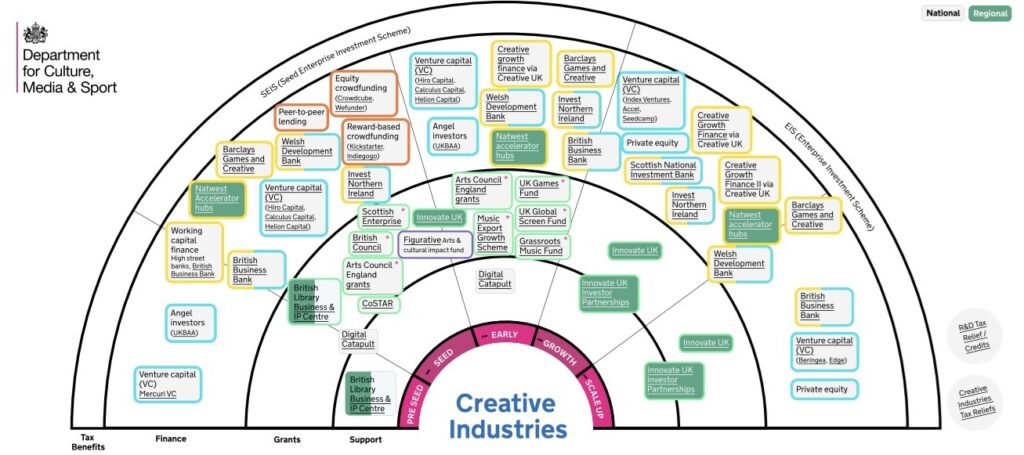

DCMS has also published new resources to help creative businesses access funding including a map of finance available to the sector, and case studies of successful creative scale-ups.

Bristol Creative Industries also a regularly updated guide to funding for creative industries businesses in the West of England here.

Click on the map for links to all the sources of creative industries funding

The creative industries account for almost a 10th of UK firms classified as having ‘high-growth potential’, and, in exciting news for our region, a lot of those businesses are in Bristol and the south west.

The report by the Creative Industries Policy and Evidence Centre (Creative PEC) and Beauhurst found there are almost 6,000 high-growth potential firms (HGPFs) operating across the creative industries. This is 9.7% of the UK’s total HGPFs and it compares to 5.1% and 2.4% respectively in life sciences and advanced manufacturing.

While London accounts for half of creative industries HGPFs with 2,942 firms, the report said other regions are home to significant numbers including 362 in the south west and, when looking at the top local authorities by number of creative industries HGPFs, Bristol is in 9th place with 129.

Over two-thirds (3,981) of creative industries HGPFs operate in application software, with significant numbers too working in marketing, branding and advertising, films and TV and video games.

The report said the figures show there is “huge untapped investment potential” for the UK’s creative industries, which currently face many challenges when it comes to funding.

The number of equity deals for creative industries HGPFs fell by 16.5% between 2021 and 2024, compared to drops of 6% for life sciences, 14% for advanced manufacturing HGPFs and 30.6% for the economy as a whole.

Creative PEC estimated there’s an equity gap of up to as much as £1.4 billion in potentially unmet demand in the creative industries.

Creative businesses also face structural challenges in relation to debt finance, the report said. They are more generally are more likely to have asset bases that are made up of intellectual property, brands and other forms of intangible capital which banks and lenders are less likely to accept as collateral.

This is shown by data which found that only 4% of creative industries HGPFs have secured debt finance compared with 6.1% and 6.2% of life sciences and advanced manufacturing HGPFs respectively.

The report highlighted Bristol Creative Industries member Watershed, which operates an independent cinema and supports creative technology, film, and media projects, as an example of how funding can work for the creative industries.

It said Watershed has received multiple grants from Arts Council England and Innovate UK, including £2.3 million grant from the Arts Council’s Grants for the Arts in 2022.

Its most recent Innovate UK grant was £1.2m in 2021 to support the MyWorld programme, led by the University of Bristol, which develops R&D infrastructure and new talent for immersive media in the Bristol and Bath region.

Additionally, MyWorld, also a Bristol Creative Industries member, is backed by a £30 million UKRI Strength in Places Fund award, which the report said illustrates how place-based UKRI funding and Innovate UK project grants specifically often work together.

Hasan Bakhshi, director of Creative PEC and report co-author, said:

“There are somewhere between 260,000 and 270,000 firms in the UK’s creative industries but not all of them have the same growth potential. Our research estimates that within this population are a vital group of almost 6,000 businesses that have especially high-growth potential.

“Given the UK’s well-known strengths in IT, it won’t be surprising to investors that the majority of these firms operate in software, but less well known will be that as many as 30% of creative industries high-growth potential firms working in software work in sub-sectors like advertising, films and TV, video content and video games too.

“This suggests that investors may identify significant new investment opportunities if they include the creative industries within the scope of their prospecting activities. Growth-focused policymakers for their part should consider the needs of high-growth potential creative industries firms in their regions.”

Baroness Shriti Vadera, co-chair of the Creative Industries Council, said:

“This research fills a critical gap in the evidence base, making clear that there are substantial untapped investment opportunities in the UK’s high-growth creative industries – across a wide range, from advertising, films and TV to video games and software.”

Tom Adeyoola, executive chair of Innovate UK, added:

“This is an important report as we aim to drive economic growth and ensure a thriving creative industries sector. This helps us understand who and where the high potential businesses are, the conditions for success and how to target the interventions needed to drive our breakthrough ideas to global greatness.”

For the latest available funding for creative businesses, read our guide.

Find lots of great creative industries businesses in our member directory.

In summer 2021 we ran an event discussing funding for creative businesses with the south west team at Innovate UK EDGE and a group of Bristol Creative Industries members.

During the discussion, attendees said it would be useful if we could provide regular updates on the finance schemes that are available for creative companies in the south west and beyond. This guide is our response.

The guide is one of Bristol Creative Industries’ most popular ever blog posts. We keep it updated with the latest funding schemes for creative businesses so check it regularly. We also include the post in our monthy email newsletter, BCI Bulletin. To sign up, go here.

Funding news:

The West of England is one of the government’s priority areas for the creative industries and the West of England Combined Mayoral Authority will receive £25m of the funding to support the region’s creative industries through the Creative Places Growth Fund.

The funding will run for three years from April 2026. Read more details about the fund here.

SMEs can apply for 50% match‑funded grants contributing toward projects valued between £20,000 and £80,000.

Funding can be used to address specific challenges or opportunities, such as adopting new technology, developing new products or services, or increasing operational capacity. The grants aim to support growth activity for SMEs from the UK government’s eight high-growth, high-potential sectors, known as the IS-8:

All funded projects must create at least one full-time equivalent role per £10,000 of grant awarded, ensuring meaningful economic impact for the region.

Eligible businesses must:

Applications close at 12pm on 12 March 2026. Companies need to complete an expression of interest prior to receiving an application pack.

The British Business Bank, the government-owned business development bank, has launched the £200m South West Investment Fund (SWIF) “to help address market failures by increasing the supply and diversity of early-stage finance for UK smaller businesses, providing funds to firms that might otherwise not receive investment”.

Aimed at businesses in Bristol, Cornwall and the Isles of Scilly, Devon, Dorset, Gloucestershire, Somerset and Wiltshire, the fund provides:

SWIF is managed by four fund managers:

The region is split as follows:

North of the region:

South of the region:

The funding is split as follows:

Businesses can apply for funding directly to the relevant fund managers here.

Grants of £2,500 to £10,000 are available to help small businesses, sole traders, charities, community interest companies (CICs), community organisations and creative and cultural groups open new premises.

The deadline for applications is 11.59pm on Monday 30 November 2026.. If all available funding is allocated before the deadline, the scheme may close early.

Successful applicants must start trading from the funded property by Friday 26 February 2027.

This £35m Creative UK and Triodos Bank investment fund provides loans of £100,000 to £1m.

Finance is directed to post-revenue creative businesses presenting promising growth potential and who:

PRS Foundation offers various grant funding schemes for music creators and organisations, including The Open Fund for Music Creators and The PPL Momentum Music Fund for artists/bands to break through to the next level of their careers.

The Black Artists Grant, offered by Creative Debuts, is £500 no-strings attached financial support to help Black artists.

The fund is an open access programme for arts, libraries and museums projects.

Funding of between £1,000 and £100,000 is available.

Loans of between £100,000 and £1.5m to UK charities and social enterprises based in England, Wales and Scotland.

Funding of between £20,000 and £50,000 for social enterprises grow. Repayments are based on a percentage of revenue so if revenue falls, repayments reduce.

This fund from Arts Council England supports individual cultural and creative practitioners in England thinking of taking their practice to the next stage through things such as: research, time to create new work, travel, training, developing ideas, networking or mentoring.

Grants of between £2,000 and £12,000 are available.

The next round of funding will open to applications in April 2026.

The £5m Supporting Grassroots Music fund supports rehearsal and recording studios, promoters, festivals, and venues for live and electronic music performance.

The Four Nations International Fund helps artists and creative practitioners from England, Northern Ireland, Scotland and Wales collaborate with each other and with partners around the world.

Th deadline to apply is 2pm on Wednesday 25 February 2026.

Travelwest provides match-funded grants for initiatives that improve sustainable travel provision in a business.

The aim is to provide financial support and incentives to employers to enable them to encourage sustainable modes of commuting or in-work travel (including site visits and meetings) amongst their staff.

The grants can be used for the implementation of physical measures, promotional events or any other measure that will encourage mode change amongst staff.

Grants are currently availables for businesses in Bristol and North Somerset.

Innovate UK’s £100m BridgeAI programme aims “to help businesses in high growth potential sectors such as creative industries, agriculture, construction, and transport to harness the power of AI and unlock their full potential”.

The programme offers funding and support to help innovators assess and implement trusted AI solutions, connect with AI experts, and elevate their AI leadership skills.

This fund supports organisations who work at the intersection of art and social change. It offers grants between £90,000 and £300,000 over three years.

Applications are currently closed but details of the next round will be announced soon.

This new £23m social impact investment fund is for socially driven arts, culture and heritage organisations registered and operating in the UK. It offers loans between £150,000 and £1m repayable until May 2030.

The Elephant Trust says its mission is to “make it possible for artists and those presenting their work to undertake and complete projects when frustrated by lack of funds. It is committed to helping artists and art institutions/galleries that depart from the routine and signal new, distinct and imaginative sets of possibilities.”

Grants of up to £5,000 are available. The next round of funding opens on12 March 2026, with a deadline of 12 April 2026.

Grants of up to £100,000 are available for arts, libraries and museums projects.

The grants support a broad range of creative and cultural projects that benefit people living in England. Projects can range from directly creating and delivering creative and cultural activity to projects which have a longer term positive impact, such as organisational development, research and development, and sector support and development.

The UK Global Screen Fund (UKGSF) is designed to boost international development, production, distribution, and promotional opportunities for the UK’s independent screen sector. It has the following schemes:

This fund aims to grow exports and global demand for UK independent film by supporting the UK film industry to achieve measurable results which would not have been achievable without the support.

Applications close on at 11.59pm on 31 March 2028.

This scheme supports the festival launch of UK films in order to enhance their promotion, reach and value internationally.

Applications close on at 11.59pm on 31 March 2028.

Supports UK producers to work as partners on international co-productions and help create new global projects.

The next round of funding is due to open for applications in February 2026.

A Start Up Loan is a government-backed unsecured personal loan for individuals looking to start or grow a business in the UK. Successful applicants also receive 12 months of free mentoring and exclusive business offers.

All owners or partners in a business can individually apply for up to £25,000 each, with a maximum of £100,000 per business.

The loans have a fixed interest rate of 6% p.a. and a one to five year repayment term. Entrepreneurs starting a business or running one that has been trading for up to three years can apply. Businesses trading for between three and five years can apply for a second loan.

If you’re running a creative social enterprise you may be able to access funding from UnLtd.

Finance of up to £5,000 is available for starting a social enterprise and up to £15,000 for growing a social enterprise.

Successful applicants also get up to 12 tailored business support plus access to access to expert mentors and workshops.

Businesses can apply for up to £3,500 to cover the costs of installing gigabit broadband.

Check if the scheme is available in your area here.

Grants to provide support towards the costs of the purchase, installation and infrastructure of electric vehicle chargepoints at eligible places of work.

The scheme covers up to 75% of the total costs of the purchase and installation of EV chargepoints (including VAT), capped at a maximum of £350 per socket and 40 sockets across all sites per applicant.

The deadline for applications is 11.59pm on 31 March 2026.

This grant supports the uptake of electric vans and trucks. It currently offers discounts up to £2,500 for small vans, £5,000 for large vans, £16,000 for small trucks, and £25,000 for large trucks.

On 18 August 2025 the government announced the plug-in van and truck grant has been extended until 2027.

If you know of another scheme that we haven’t listed and you’d like to share it with other creative businesses, email Dan to let us know.

The primary goal of any filming day is the final polished video. But the true story of innovation, teamwork, and expertise often lies in what happens between the takes. This is the power of a well-executed Behind-the-Scenes (BTS) strategy.

BTS content delivers three key advantages:

– It showcases your people. BTS content captures the personalities and passion behind your brand. It’s about trust, collaboration, and the shared goal of creating something great.

– It builds audience trust by offering a transparent look at your process, showcasing the technical skill and planning involved.

– It fuels your marketing. A single filming day can provide a treasure trove of authentic photos and video clips to keep your social media channels buzzing for weeks.

Case study in action: Our recent shoot with Hot Robotics and the University of Bristol for their Cerberus robot project is a perfect example.

The accompanying BTS film (shared below) goes far beyond a simple “making-of.” It captures the reality of a complex shoot: setting up the master interview ‘studio’, coordinating drone on drone aerial sequences, fun with smoke pellets and, of course, the obligatory trip to Greggs! All the while maintaining a fantastic team dynamic.

This footage becomes an invaluable asset, demonstrating both technical capability and a strong collaborative culture.

You are currently viewing a placeholder content from YouTube. To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

Bristol, UK – January 2026 — Ignition DG Ltd, the Bristol-based strategic events and exhibitions agency, as part of Istoria Group, today announces significant business growth. From expanded global reach to continued leadership, Ignition DG continues to generate impressive results in the sector.

Founded in 2007 with a mission to challenge traditional “build and burn” event practices, Ignition DG has grown into an award-winning creative agency known for blending strategic planning with world-class delivery.

Global Growth

Ignition DG designs and delivers hundreds of exhibitions and event programmes each year – serving clients across pharmaceutical, beauty, biotech, aerospace and technology sectors.

To support recent successes, Ignition DG ended 2025 with the opening of a new European office. With strategic hubs and warehouse facilities now established across the UK, EU and the US, Ignition’s global growth goes from strength to strength. Paired with trusted partners across Asia, the Middle East and South America, the business has consolidated its ability to support global programmes with local expertise.

Client Success

From complex exhibition portfolios and major congresses, Ignition’s work emphasises strategic intent, creative innovation, and seamless project management – underpinning sustained client retention and growth.

Alongside continued client success, Ignition has won awards for booth designs, creative event executions, and bespoke modular solutions that deliver high impact and cost efficiencies for global brands.

With recent client wins, Ignition has attracted new talent to the company, seeing a 19% increase in employees throughout 2025.

Innovation Through Change

In recent years, the company has responded to shifts in the events landscape by scaling its digital and hybrid capabilities. This adaptability has reinforced client partnerships, enabling Ignition DG to deliver hundreds of virtual events and hybrid programmes that seamlessly blend creativity with technology.

Innovation continues to be part of Ignition’s DNA. New strategic capabilities, such as building exhibition attractors in-house, are being launched, alongside medical content writing as a service.

Looking Ahead

“We’re proud of the sustained growth we’ve achieved while staying true to our founding values,” said Sam Rowe, CEO of Ignition DG. “Our team’s focus on creativity and strategic excellence has allowed us to support clients around the world with meaningful, measurable experiences.”

With continued investments in strategic solutions, talent and technology, Ignition DG is poised to grow further into 2026 and beyond. The company remains committed to helping clients across regulated industries to create impactful live experiences that drive business results without compromising environmental or ethical standards.

For media enquiries, please contact:

[email protected]

Chase Design Group is expanding its Western European presence with a move to a larger space in Bristol, UK, and the promotion of key leaders who will guide the agency’s continued growth and partnerships across the region.

Chase Design Group is an independent creative agency with offices in Los Angeles, New York, and the UK, with expertise across brand strategy, identity development, package design, and retail environments.

Shannon Osment has been promoted from Director of Accounts to Managing Director, Chase Design Group. Shannon began her career in Chase Design Group’s Los Angeles office in 2004, and single-handedly established its UK presence in 2017. With 20 years of experience in brand identity and consumer packaged goods, she has led teams in transforming global brands such as Procter & Gamble, L’Oréal, and Unilever. Passionate about people and driven by curiosity, Shannon finds fulfillment in building both strong brands and strong teams as she now leads the studio and mentors emerging talent.

Pete Hawkins, who joined Shannon in the UK office in 2018, has been promoted from Creative Director to Group Creative Director. He brings over 20 years of experience across many sectors, from banks to beers, while his approach blends strategic design thinking, original creative ideas, and meticulous craft to deliver impactful, intelligent solutions. He thrives on building strong, open partnerships with clients and creative teams alike, believing that the best work emerges from shared vision, curiosity, and trust.

With a team that has grown to 15 people, the new, expanded office is closer to the city of Bristol and is focused on growth across Western Europe.

According to Chris Lowery, CEO, Chase Design Group, “In addition to their new global responsibilities, we welcome Shannon and Pete’s cross-studio leadership voices as they help us grow and expand into new territories.”

You need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More Information