Between 2026 and 2029, up to 12 challenge calls will be identified where innovative new thinking could catalyse a step change in the industry, while producing learning and insights that benefit the whole screen sector.

Synergist is the software that helps agencies run better. Connecting projects, resources and financials in one place, so agency leaders can see exactly what’s happening in their business and make smarter decisions.

Agency Works are the software implementation experts behind some of the UK’s best-run agencies. Helping creative businesses get Synergist properly embedded, configured to the way they work, and delivering real results from day one.

For years, our two businesses have worked side by side, sharing the same purpose: to make a real difference in how agencies run and elevate their performance.

So when the opportunity came to make it official, to bring both teams together under one roof, it felt less like a big decision and more like the obvious one. There was really only ever one question: when?

Now, they’re making it official. Synergist and Agency Works are becoming one business, and have joined Banyan Software — a group that acquires and backs successful software businesses for the long term, keeping teams in control while giving them the support to grow.

Jay Neale, CEO of the combined business, said:

“This has been a long time in the making. Our two teams have always shared the same purpose: helping agencies be their best and enjoy the ride. Becoming one business simply made sense, and finding a home for life with Banyan gives us the support to deliver even more for our clients. I’m incredibly proud to be leading the combined business as CEO, and with Banyan behind us, I genuinely believe the best is still to come.

Nick Lane, Chief Operating Officer of Synergist, said:

“Synergist has been built over more than 20 years on the trust of the agencies we serve. This doesn’t change that. If anything, it strengthens it. Same product, same people, same purpose. Now with more resource and backing behind us, we can build faster and go further for our customers than ever before.”

For existing clients and users, nothing changes day to day. With more resource and backing behind the combined business, the focus is on building faster, delivering better, and continuing to improve the software and services agencies rely on.

For agencies considering Synergist for the first time, you’re not just getting software. You’re getting 25 years of agency expertise built into a platform, configured by people who’ve worked in agencies themselves and know the challenges inside out.

The best is still to come. Two brilliant teams, one shared purpose, and more firepower than ever to deliver on it.

From pipeline to profit. Synergist connects your projects, resources, and financials in one place – streamlining work and giving you the management data you need.

Spot capacity bottlenecks before they happen. Understand exactly how time is utilised. Track which clients are profitable. Know where you’re losing money. See problems coming, make smarter moves, run your agency on reality not guesswork.

It’s not just software. It’s 25 years of agency expertise built into a platform that flexes to your needs, configured by experts who know agencies inside out. They’ll match it to your processes, challenge what’s not working, and support you as you scale.

The UK’s leading agency software for agencies that want to scale profitably.

To find out more or book a demo, visit synergist.co.uk

Compiled by Sarah Williamson, Content Marketer and Leah Disley, Brand Photographer

Location matters more than you might realise, because it does more than “look nice”. It shapes how your brand is perceived, how confident you feel during the shoot, and how versatile your images are long after shoot day. The right setting can help your photos feel professional, natural and versatile — images you actually want to use across your website, email marketing and social content, not just once and forget about.

Whether you’re a service provider building a personal brand, launching a new offer, or refreshing your visuals, Bristol is a brilliant city for brand photography because it offers two very different things:

In this guide, I’m sharing fifteen of the best places for a brand photoshoot in Bristol, all photographer-approved and chosen specifically for how well they support business-focused shoots.

Free, flexible and unmistakably Bristol. These locations are ideal if you want your photos to feel natural, relaxed and rooted in the city.

Outdoor shoots are great if you want:

One of Bristol’s most underrated brand shoot locations.

Brandon Hill offers leafy paths, open lawns and beautifully kept gardens, giving you a soft, natural backdrop that feels calm and timeless. You can give the greenery a starring role or include Cabot Tower subtly for a recognisable but understated Bristol reference.

Best for: Service providers wanting a natural, grounded feel without going fully “woodland”.

One of Bristol’s most visually dynamic areas.

Water reflections, boats, converted warehouses and colourful buildings give you depth and movement. Within a short walk, you can capture several distinct looks.

Best for: Brand shoots with energy, editorial shoots, creative portraits and lifestyle imagery.

Ashton Court offers scale, variety and atmosphere all in one location.

With woodland paths, open fields, rolling hills and a historic mansion, you can capture multiple looks without moving locations. Natural light here is consistently flattering, especially later in the day.

Best for: Lifestyle branding, natural portraits and shoots that benefit from space and movement.

Bold, creative and constantly evolving, Stoke Croft is Bristol’s creative heartbeat.

The murals and street art everywhere you look create instant visual impact without needing props or styling. The ever-changing street art means no two shoots look the same, and the area offers endless creative angles.

Best for: Creative brand shoots, bold brands and anyone wanting personality-led visuals.

Open, airy and timeless.

With wide green spaces, wild grasses and trees, the Downs offer a variety of natural backdrops that feel open, soft and easy to work with. Soft morning light and golden hour here are particularly flattering, and the space allows for relaxed, natural shooting.

Best for: Natural brand portraits, candid portraits and lifestyle imagery.

The full Bristol moment.

If you love the bridge and want drama, this is it. The scale and backdrop are unmatched, especially in good light.

Best for: Statement shots and strong hero images.

A tranquil woodland setting on the edge of the Avon Gorge.

Dense woodland, dappled light and natural textures create depth and softness. From certain angles, you can catch subtle glimpses of the Suspension Bridge without it dominating the frame.

Best for: Storytelling photography, lifestyle branding and nature-inspired shoots.

Iconic without the climb.

Sion Hill offers a clear, impressive view of the Clifton Suspension Bridge behind you, without the hike required for St Vincent’s Rocks. It’s a cliché for a reason — it works.

Best for: Anyone who wants unmistakably Bristol visuals with minimal effort.

A Bristol institution.

The colourful houses on this quiet street create a bold, urban backdrop that feels lived-in and real. It’s instantly recognisable to locals without feeling like a cliche.

Best for: Personal brands that want warmth, colour and an urban edge.

A bonus location for colour lovers.

The row of colourful houses looks fantastic from across the river. Shooting from near Thekla or the Redcliffe Bascule Bridge gives you layered compositions with water, colour and architecture.

Best for: Creative brands and lifestyle-led shoots with visual interest.

When you want privacy, consistency and full control — regardless of the British weather!

Indoor shoots are ideal if you want:

If you’re looking for a clean, light-filled indoor space for a brand photoshoot in Bristol, The Engine Room is hard to beat.

The Engine Room is a bright, versatile indoor studio with a large 60 m² main space, high ceilings, crisp white walls and a neutral grey floor. This makes it ideal for shaping light and styling shoots without distractions.

Natural light floods in through full-height glass doors and a lantern skylight, giving the space an open, airy feel that works beautifully for personal brand portraits, product photography and video content.

There’s also an adjoining Green Room for outfit changes, prep time or makeup, plus ground-floor access, free parking and reliable Wi-Fi — all of which make shoot days smoother and less stressful.

Best for: Personal branding, studio portraits, editorial content, product photography, flat lays and video shoots where control and consistency matter.

Gather Round’s production space offers a private, flexible indoor environment right in the heart of Bristol.

The production space offers a controlled, indoor environment with blackout capability and a private entrance, making it ideal for focused shoots.

Best for: Studio portraits, creative product photography, editorial work and campaigns that need a controlled indoor setting.

One of Bristol’s largest and most professional creative studio spaces.

With over 10,000 sq ft of purpose-built studios, including soundproofed spaces and an infinity cove, this is ideal for high-production shoots that need room to breathe.

The facilities go beyond just empty space. Green rooms, makeup and wardrobe areas, breakout spaces and on-site equipment hire make full-day shoots far more efficient.

Best for: Fashion editorials, commercial campaigns, product photography, interviews and brand shoots requiring a professional studio setup.

Full production-level facilities.

Large studios, soundproofing, infinity cove (seamless studio backdrop) and on-site equipment hire make this ideal for higher-production shoots.

Best for: Commercial campaigns and high-end brand shoots.

Compact, creator-focused and efficient.

A small but well-equipped studio with good lighting and a clean setup, making it easy to capture polished, professional imagery without distractions.

Best for: Headshots, talking-head videos, product photography and social content creation.

Choosing the right location is only part of the puzzle. Knowing what to shoot — and how those images will support your business — is what turns a photoshoot into a real marketing asset.

That’s exactly why we created the Brand Compass Edit.

Hosted at The Engine Room in Brislington, it combines a professional brand photoshoot with content guidance, so you walk away with images you actually know how to use across your website, emails and social content.

If you’re planning a brand photoshoot in Bristol and want visuals that work beyond the shoot day, this is your next step.

A deep dive into the UK branding and marketing market from the perspective of independent agencies

(link to full article including interactive heatmap)

Clide Research | February 2026 | getclide.com

When an agency achieves the remarkable feat of 7-digit revenue, the owners (and their teams) are often not content with continuing as a lifestyle business and want to grow further into 8-digit.

A larger agency is not just about more revenue; domain authority does deliver premium pricing (30+%) and better profit margin (5+%).

This is rarely achievable by “doing more of the same”, especially in a market dominated by large global networks at the top. Most agencies try a lot of ideas, which brings the challenge — there are often more ideas than the resources available.

We studied the growth paths of hundreds of UK agencies to analyse what propelled them to 50-100+ people organically, not to offer a playbook, but to illuminate the proven paths and help agency owners anchor their thinking.

The analysis revealed intriguing patterns:

We identified 4 structural changes that independent agencies could seize next 1-3 years, driven by AI adoption and key regulatory changes.

The report concludes with a high-level framework for agency owners to identify the 2-3 strategic bets that best suit them, and how to narrow down to a winning bet.

Getting an agency to seven figures is genuinely hard. Most new agencies never manage it. You survived the project feast-and-famine of the early years, built a team you trust, developed a body of work you are proud of, and found enough clients who value what you do to sustain something real.

The success also means your team no longer just show up to do a job, they gather because of your vision, and what it could mean for their futures. The anticipation for further growth is strong.

You have no shortage of idea. That creative, entrepreneurial instinct is precisely what built the business. It generates hypotheses constantly: a new sector to target, a new service to offer, a new positioning to test, a new market to enter.

The problem is not the ideas. It is the fact that you cannot try everything.

When many ideas are pursued, experiments multiply. The team follows each new direction with diminishing energy. The founding partners become stretched across too many fronts.

This is a familiar pattern at the seven-figure level, and it is not a failure of ambition or effort. It is the natural consequence of a business growing beyond its original design.

Large company chief executives solve this differently. They also face resource constraints and uncertainty, and they invest efforts into identifying a small number of strategic bets that suit their organisations. It’s followed by clear evaluation and aggressive narrow down based on evidence. This approach feels like a luxury when you are building from zero. When you are running a team of twenty or thirty people, it starts to become a necessity.

That is what this article is designed to support. It does not offer simplistic playbooks. It offers a structured view of the UK market from the independent agency perspective, and draws from hundreds of case studies to illuminate the proven paths.

The goal is to help you build conviction from evidence — and then commit to it.

KEY INSIGHT The UK agency fee pool is £8-12bn, but is dominated by large global networks. However, enterprise buyers increasingly prefer best-of-breed capabilities, providing opportunity for well-positioned independents to capitalise.

The UK advertising and marketing market generated £42.6 billion in total spend in 2024, according to the AA/WARC Expenditure Report, and is expected to grow by c.10% per year.

But much of this number is not relevant for independent agencies.

75-80% of this is media spend: the cost of buying airtime, ad space and search/social placement. That money flows through agencies in many cases, but it does not represent fees earned for thinking, creating, or advising. The actual fee pool for branding and marketing services is estimated in the region of £8 to £12 billion.¹

Within this fee pool, the global networks like Omnicom/Interpublic, WPP, Publicis, Havas and Dentsu dominate, by holding the agent-of-record relationships with the largest spenders.

That said, independent agencies have consistently carved out a corner — the top 50 UK independent agencies generated £2.23 billion in the most recent survey year.³ Opportunities usually come from two sources.

Enterprise customers increasingly prefer best-of-breed capabilities on specific areas (e.g. product launches, customer communication, etc.). This opens a wide spectrum to attack for agencies with unique creative philosophy, deep audience understanding or channel expertise.

Most established independent agencies built their businesses in this space and there is a continuous supply of opportunities for up-and-coming agencies. To name a few recent examples:

In each case, the independent agencies provided specialist depth that the networks could not match on that specific brief.

Global networks don’t tend to pitch for customers with <£500k annual fees, constrained by the overhead costs in their business models. This floor is likely increasing due to persistent cost inflation.

This market is collectively large, but the challenge is finding consistent spend streams. The companies in this segment are typically smaller and do not spend consistently on brand strategy and creatives. However, some sectors do reliably spend on communication (e.g. financial services) and downstream marketing services (most B2C sectors).

KEY INSIGHT Financially, scaled agencies are not just bigger versions of smaller agencies. They earn more per person, hold structurally better margins, and have materially more options — including the choice of whether to remain independent.

The 2025 Moore Kingston Smith Annual Survey of UK Marketing Services Companies reveals a clear and consistent gap between group-owned agencies — those within network or PE structures — and independent agencies.

Fee income per head averaged £130,072 at group-owned agencies against £100,926 at independent agencies.³ That is a 29% premium in revenue productivity. At the size where this gap opens up, it is not a marginal difference — it is the difference between a business that generates surplus capital and one that does not.

The margin picture tells a similar story. High-performing agencies — defined as top-quartile for both revenue growth and operating profit — achieved a margin threshold of 18.2%. The industry average operating profit margin was 10.2%.³

These numbers are not benchmarks to aspire toward vaguely. They are a description of what a different business model — one built on specialist positioning, recurring client relationships, and pricing power derived from genuine expertise — actually produces financially.

The mechanism is compounding rather than linear. Specialist positioning commands higher fees. Higher fees fund better hires. Better hires deepen the expertise that justified the premium. Deeper expertise attracts stronger clients, who tend to extend relationships and commission broader scopes of work. Broader scopes generate recurring revenue. Recurring revenue produces more consistent margins.

Each element of that sequence reinforces the next. The agencies that broke through to 100 people did not do so by doing more of what they were already doing. They did so by reaching a position where the compounding effect kicked in — where sector or audience depth was deep enough to justify premium pricing, and premium pricing was sufficient to fund the next hire that deepened the moat further.

KEY INSIGHT Most combinations of sector and specialism could not support an independent agency reaching 100 people. A small number of combinations have consistent examples. The shape of that pattern is not random — it reflects where client spending is large enough, repeatable enough, and specialist enough to support scale.

We studied hundreds of UK agencies and mapped the growth path of 100+ that achieved 50+ people in scale. The analysis focuses on what propelled each agency into scale during its independent phase. Many of these agencies have since been acquired and have expanded into multiple specialisms under network or PE ownership. What matters for this research is the positioning and model that created the foundation — not what the agency became afterwards.

We divided the market into 13 sectors and 11 disciplines. For each growth story, we asked two specific questions:

The heatmap makes the patterns visible. The majority of sector/discipline cross-sections did not consistently produce large agencies. This does not mean opportunities do not exist there — plenty of <50 people agencies built sustainable businesses. It just shows the larger market forces and client spend patterns historically did not support independent scale.

Important: the heatmap does not prescribe a formula. Every growth story has its own ingenuity and market backdrop; it’s too much to cover everything in this report, so we focus on the patterns in the results.

KEY INSIGHT The agencies that scaled all demonstrated strong discipline focus, they occupied positions where the market structure — client budget size, brief repeatability, knowledge barriers to entry — could support a large independent specialist. The breakout opportunities were often presented during significant changes in their target markets.

The heatmap shows five patterns that can be useful for agency owners’ thinking.

The agencies that reached 100 or more people consistently built around a specific positioning — a sector, a channel, a specific audience type, or a defined part of the value chain. Agencies that remained generalist rarely scaled.

This is not a coincidence. Specialist positioning does several things simultaneously: it commands higher fees than generalist alternatives; it creates genuine switching costs as the agency’s knowledge of the client’s world becomes embedded; it builds a reputation within a specific community that makes new business more efficient; and it provides a clear basis for senior hiring. Generalist agencies compete on execution and relationships. Specialist agencies compete on knowledge — and knowledge compounds in ways that execution does not.

FMCG, financial services, technology, and healthcare supported the largest number of scaled agencies. Other sectors attract significant agency activity without producing a meaningful number of agencies reaching 50 people or more.

Property, sports, education, and gaming all show this pattern. Strong creative communities exist. Talented agencies work in these sectors. But no consistent pattern of sizeable independent specialists has emerged.

They share common characteristics: client budgets are smaller or less consistent; brief types lack the volume and repeatability that supports a large team.

The heatmap makes this visible. For anyone considering a deliberate sector bet, this is important information — not a reason to dismiss the opportunity entirely, but a signal that the structural conditions may be working against you.

Looking across the last 3 decades, independent agencies have been consistently fast at capturing, and dedicating to, structural shifts in the broader economy. And such focus is frequently rewarded with scale.

In almost all of these cases, the work they delivered was already covered by existing agencies, but they brought a sharp focus that won the market over. For example:

With the exception of performance marketing, we found no visible examples of an independent UK agency reaching 100 people by focusing primarily on mid-market clients. Even startup-focused Koto has since expanded into digital-rebranding for enterprise customers.

This is a meaningful finding, because the mid-market is where many independent agencies get their early new business. Mid-market clients have smaller budgets, typically want a broader range of services than a specialist can efficiently provide, and tend to be more price-sensitive.

The agencies that scaled worked with large companies — often ones where global networks were also present on different parts of the account. The independent won a specific mandate, not the whole relationship. The brief was large enough to justify the expertise, and the client was sophisticated enough to value it.

This does not mean mid-market clients have no role. They are often where the specialism is first developed and proven. But scaling required moving up the client tier, not across it.

Brand strategy is a frequently used phrase to encapsulate the work by an agency. Intriguingly, very few agencies have reached scale by focusing on brand strategy/architecture alone (with limited/no creative), almost none in recent years.

This reflects the traditional high value segment for brand strategy (brand transformation, mergers & acquisitions driven brand consolidation, major rebrand) is increasingly taken by large global networks; yet the brand strategy spend by smaller companies is not sufficient to support an agency at scale.

There are smart angles such as Brand Finance turning brand valuation into a product (WPP has similar capabilities, but used more internally), but that’s more an exception than a pattern.

KEY INSIGHT The agencies that scaled built positions where the pricing power lived in their thinking, not their production. All three growth architectures involve execution capability — but in each case, the execution is the delivery mechanism for specialist knowledge, not the source of the value.

Across the agencies that exceeded 50 or more people independently, three distinct growth architectures emerge.

The growth paths across the architectures are similar. Deep knowledge commands premium fees. Premium fees fund specialist hiring. Specialist hiring deepens the moat. A deepened moat attracts international clients — and international clients create the natural demand for a second studio, which is typically the inflection point that changes the growth trajectory from linear to compounding.

These agencies consistently sold downstream into implementation as they scaled — packaging production, communications delivery, campaign execution — creating significant revenue volume on top of the strategic and creative fees. But their downstream offering is focused on their specialty, avoiding significant ballooning of headcount usually associated with downstream services.

An agency that builds institutional knowledge in a specific industry sector, and tangibly tailors how it approaches its specialist discipline — the clients regard it not as experienced, but as genuinely expert. The moat is the knowledge and demonstrable approach, perpetuated by a growing roster of highly relevant case studies.

The knowledge starts to live in the agency’s processes, methodologies, and people — not just in the founder. That is what makes it scalable.

This architecture is most commonly observed in creative and communications specialisms. Creative specialists focused on FMCG and consumer brands produced the most successes, for example:

Financial services communication specialists produced the second largest cohort of scaled agencies, for example:

Technology corporate communications specialists produced the third largest cluster, for example:

Healthcare and pharmaceutical is also worth a mention, supporting multiple communications specialists to above 50 people (e.g. Madano, Hanover Communications, etc.) and helped Lynx grow to 400 people.

Deeply expert in a specific audience type: consumers, investors, employees, a particular demographic or cultural community. Many scaled agencies focused further on an audience type within a sector (e.g. financial services shareholders).

The moat is built on audience insight and a methodology that’s visibly tailored for the audience. The positioning is: we know how to speak to this audience — and that understanding is proprietary, systematic, and often transferable across client sectors.

Some notable examples:

The audience-focused model is one of the most dynamic over time, heavily driven by the way people consume information and generational shift.

The sophistication of search and social channels increased in line with the rising usage by advertisers; extracting optimal performance started to require deeper channel-specific expertise.

Unlike traditional media buying, the concentration of the channels created large execution-focused agencies. It’s also one of the rare examples where mid-market clients provided growth engines given their significant and consistent performance marketing spend.

The winners are focused on data but also have knowledge about content-channel fit and deploy proprietary software to link campaign management data to the client’s systems. They usually work alongside creative firms, delivering content rather than creating it.

Scaled agencies in this model usually have high headcount (large offshore workforce to handle manual processes), some examples:

KEY INSIGHT The agencies that scaled most dramatically did not do so only through internal excellence. Their growth was typically punctuated by structural market changes that created demand for specific capabilities at the right moment. Multiple structural changes are unfolding in the UK in the next 1-2 years.

As we discussed in Section 4, seizing structural changes in the market has created a large number of scaled agencies.

Looking further back in history, this pattern holds extremely well. FMCG packaging specialists scaled on the back of globalisation. As brands expanded from domestic markets to international portfolio management in the 1990s and 2000s, the agencies that had built the deepest expertise in brand design and packaging found that the same global clients who valued their work in the UK needed it replicated in Amsterdam, New York, and Singapore. The agencies that followed their clients into new markets grew significantly larger than those that did not.

Healthcare communications specialists scaled on pharmaceutical deregulation and the global clinical trial boom of the same era. Corporate communications agencies scaled on the privatisation waves of the 1980s and 1990s, and more recently on the rise of ESG disclosure requirements that created volume demand for stakeholder and investor communications.

In each case, a structural shift in the market created conditions where a specific type of specialist expertise became substantially more valuable. Agencies already positioned in that space captured a disproportionate share of the resulting demand.

Structural changes in the UK to watch out for

Several structural changes are afoot in the UK at the moment. Below are a few that are unfolding in real time and could have systematic impacts on how companies approach branding and marketing.

UK HFSS restrictions on advertising of high-fat, salt, and sugar products — which came into force on 5 January 2026 for TV and online channels — are creating a material change in where major food and drink brands allocate their marketing budgets.¹⁴

A few reaction patterns are emerging:

Industries experiencing rapid AI-driven disruption — software, professional services, financial services, education — are under significant pressure to articulate their value proposition in a world where their investors expect their core offering to be impacted by AI. The brands that navigate this well need genuine strategic depth: the ability to reframe positioning, rebuild messaging architecture, and communicate clearly through a period of structural uncertainty.

This creates demand for strong communication capabilities and the ability to deal with the urgency of the situation (a broad spectrum of companies have suffered 20+% share price decline in the first two months of 2026). The window in which a brand can define its position in an AI-disrupted landscape is not indefinite — the categories are moving fast, and early positioning decisions will be difficult to revise.

AI chatbots have taken a visible chunk out of search activities, and the trend is likely to increase with the chatbot builders rapidly rolling out new use cases (e.g. shopping, travel planning, etc.).

This changes the way consumers access information, which will likely impact how brands communicate with them effectively:

Marketing and customer services are the first two areas that saw mass AI adoption. While this brings efficiency and gives customers a faster experience, the de-personalisation and the repetitive “AI tone” are also drawing customer resentment.

As AI adoption grows further, brands will most likely start to respond and seek to bring on-brand tones and communication approaches to their AI agents.

Multiple startups recently backed by Y Combinator are already focusing on delivering on-brand and personalised experiences via AI agent, indicating growing awareness of the issue. And Definition already lists a service that helps to tune their client’s AI agent.

KEY INSIGHT Most agency founders know what they believe they are best at, but market forces and competition could mean the commercial results look different. A commercially honest audit is the crucial foundation for strategic planning.

The market map and the three growth architectures are useful frames. But the actual paths have to be built from your own data. You have intuition about what you are good at, but that should be checked against what your business has won, charged and retained, and profited to clarify your genuine competitive advantages.

A structured way to surface that signal is to review the last three years of work through four lenses simultaneously.

Fee rates and margins by sector and service type. Where has pricing been strongest? Where have write-offs been lowest? The data almost always reveals concentrations the team has not consciously registered. If you have consistently charged more for a specific type of brief than any other, that is worth understanding.

Client lifetime value by segment. Which engagements led to extended relationships, expanded scopes, and referrals? Long-tenure clients are not just commercially valuable — they are evidence that the agency is delivering something the client cannot easily replace.

Close rate by brief type. Where does the agency win most consistently? High close rates in a specific category are a reliable signal of genuine competitive advantage. Low close rates in a category you are actively pursuing is a signal worth paying attention to.

Team energy. Which types of work generate genuine engagement from your best people? The alignment between what the team finds meaningful and what the market rewards well is the foundation of a durable position. Misalignment — strong commercial performance in areas the team finds draining — is a warning sign for sustainability.

The intersection of all four is where your positioning should be built. In most agencies at the seven-figure level, this intersection is considerably more specific than the agency’s current official positioning suggests.

Once you have identified your strongest intersection through the commercial audit, the next question is which paths you should bet on.

You are usually the main salesforce, and your time is limited, so it’s critical to identify 2-3 strategic bets that exemplify your strengths.

Home in on your star discipline, identify 1-2 sectors where you and your team feel strongly, and that have sufficient spend power. Create positioning ideas with your team that captures potential catalysts facing those sectors that you can address better than anyone else. This makes sure everyone is on the same page and attacks these angles at full energy.

No plan survives contact with the enemy. Adjustments will be necessary. That’s why it’s critical to have full visibility on progress in real time. When you feel the need to try a new angle, it means at least one of the existing angles should be shut down. This is critical to ensure you do not overstretch your resources and your own bandwidth.

Moat first. Scale follows.

1. AA/WARC Expenditure Report, April 2025 — UK total advertising expenditure £42.6 billion in 2024. Media spend proportion estimated by the authors. https://adassoc.org.uk/our-work/uk-advertising-records-42-6bn-spend-in-2024/

2. Omnicom Group and Interpublic Group merger announcement, December 2024; merger completed November 2025. Combined revenue figures per company disclosures. https://investors.interpublic.com/news-releases/news-release-details/omnicom-acquire-interpublic-group-create-premier-marketing-and

3. Moore Kingston Smith Annual Survey of UK Marketing Services Companies, 2025. https://mooreks.co.uk/insights/snapshot-annual-survey-on-the-financial-performance-of-marketing-services-companies-2025/

4. Historical analysis of Publicis/Saatchi and WPP/JWT merger periods; authors’ assessment.

5. Epoch Design company profile; client claims per company website. Employee count per 6sense and LinkedIn data, February 2026. https://epochdesign.com/

6. PMLiVE — Havas Lynx company profile and Campaign Healthcare Agency of the Year citations. https://pmlive.com/pmhub/havas_lynx/

7. Dentsu Aegis Network — Gyro International acquisition announcement, July 2016. https://www.dentsu.com/us/en/news-releases/dentsu-aegis-network-acquires-gyro

8. Emperor Design — company website and Companies House filings. https://emperor.works/about/ | https://find-and-update.company-information.service.gov.uk/company/03160710

9. Buttermilk — company website and Favikon employee data, February 2026; Unilever appointment per industry press, 2025. https://thinkbuttermilk.com/

10. Amplify — Brand Experience Agency of the Year 2024; financial figures per company announcement. https://weareamplify.com/

11. The Imagination Group Limited — Companies House filing, August 2024 accounts. https://find-and-update.company-information.service.gov.uk/company/02275977

12. Inflexion Private Equity — Goat Agency investment announcement, March 2021; WPP — Goat Agency acquisition by GroupM, March 2023. https://www.inflexion.com/portfolio/goat/

13. Brainlabs, Croud, and Jellyfish — company profiles and PE/acquisition announcements per company and investor disclosures. https://www.brainlabsdigital.com/ | https://www.croud.com/ | https://www.jellyfish.com/

14. ASA/CAP — HFSS advertising restrictions on less healthy food and drink, came into force 5 January 2026. https://www.asa.org.uk/news/new-rules-and-guidance-for-less-healthy-food-and-drink-advertising.html

Clide helps independent branding and marketing agency owners think through the strategic questions that will shape the next five years of their business.

getclide.com | © Clide 2026

Bulletproof – The Event Every Agency Owner Can’t Afford to Miss

2026 marks the third post-COVID edition of the Bulletproof Agency Network conference, and this year, we’re raising the bar.

We’re heading back to the stylish surroundings of VOCO Manchester for a day designed to challenge your thinking, sharpen your strategy, and reconnect you with what makes agency life exciting in the first place. Expect bigger conversations, deeper insights, and more meaningful connections than ever before.

The theme for 2026 is “Pitch to Partnership.”

Because winning work is only the beginning. The agencies that truly thrive are the ones that know how to turn a single opportunity into a long-term, high-value relationship. This year is about mastering that transition – from proposal to partnership, from project to profit, from client to collaborator.

Let’s be honest: running an agency can feel relentless.

You’re balancing delivery and growth. Managing people and expectations. Navigating uncertainty while trying to stay commercially sharp and creatively relevant.

Bulletproof exists for that reality.

Imagine spending a day surrounded by people who genuinely understand the pressures you’re facing, leaders who’ve made the mistakes, solved the problems, and discovered what actually works. Not theory. Not fluff. Real-world strategies, honest conversations, and practical ideas you can take back and apply immediately.

That’s the difference.

Bulletproof isn’t just another conference.

It’s a reset button for ambitious agency owners who want more. More clarity, more confidence, and more control over where their business is heading next.

Meet this year’s lineup of industry experts

This year’s conference features an outstanding lineup of speakers who’ve mastered the art of scaling businesses, leading teams, thriving through challenges and building resilient agencies.

Keynote speakers include:

Trenton Moss

Founder of Team Sterka, he puts his agency’s success down to one thing, making everyone a leader.

Katie Bolas

Ex-agency leader turned Fractional Operations Director, who helps agencies succeed by fixing the operational issues that drain profit and frustrate teams.

Claire Richardson-Critcher & Steve Byrne

Co-Founders of As The Crow Flies, they are renowned for their ability to cultivate powerful, sticky habits that create proper confidence when forecasting New Business.

Hosting the event is Dan Archer of Suprpwr Consulting, he’s all about helping businesses make marketing their Superpower.

And it’s not just the keynote talks. Attendees will dive into specialist-led sessions packed with legal, financial and insurance insights designed for the unique challenges of creative and digital agencies.

Experts such as Steve Kuncewicz (Glaisyers), Paul Barnes (MAP) and Michael Henderson (Riskbox) will be sharing their insights to help future-proof your agency.

Bulletproof isn’t just a conference, it’s a community.

This isn’t just a day of learning, it’s your chance to meet other agency owners who truly get what you do, swap stories, celebrate wins and lessons and walk away with connections that last long after the conference ends.

Grow Your Agency, Support Your Community

Bulletproof 2026 isn’t just about learning and growing your agency, it’s about making a real impact while you do it. 100% of ticket proceeds will be donated to 2 incredible local charities: Forever Manchester & Barnabus , so you can level up your agency while giving back to the community.

Join the Leaders Shaping the Agency World

After last year’s amazing day, demand is already high for Bulletproof 2026, so don’t miss your chance to be part of a day that will leave you inspired, connected and ready to take your agency to the next level.

Grab your ticket here & join us on the 7th May for an unforgettable day.

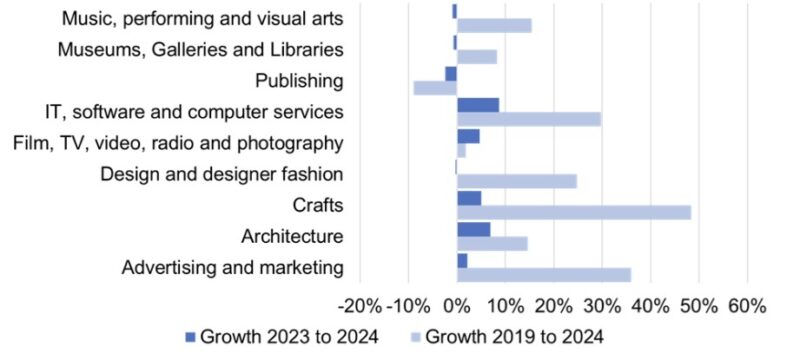

The creative industries contributed £145.8bn in gross value added (GVA) to the UK economy in 2024, new government figures have revealed.

Creative industries GVA rose by 4.6% between 2023 and 2024, compared to the UK economy as a whole which grew by 1.0%, the data from the Department for Culture, Media Sport (DCMS) shows.

The sector’s GVA was 19.7% higher than pre-pandemic (2019) and 60.3% higher than in 2010, in real terms.

The growth was driven by the ‘IT, software and computer services’ subsector which increased by an estimated 8.7%, followed by ‘film, TV, radio and photography’ and ‘advertising and marketing‘ which grew by 4.6% and 2.1% respectively.

‘IT, software and computer services’ is the largest subsector of the creative industries by GVA, contributing an estimated £62.4bn in 2024. ‘Advertising and marketing’ is the next largest with £24.3bn.

Growth in creative industries subsectors, in chained volume measures (CVM):

Other data released this month showed the creative industries account for almost a 10th of UK firms classified as having ‘high-growth potential’, and a lot of those businesses are in Bristol and the south west.

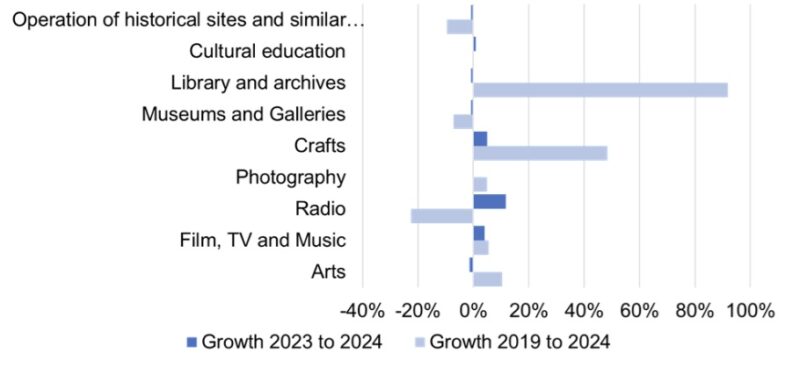

The DCMS report also included data for the cultural sector which contributed an estimated £40.3bn in 2024, accounting for 1.5% of UK GVA.

GVA grew by around 2.4% from 2023 to 2024, compared to the UK economy as a whole which grew by 1.0%. From 2010 to 2024, culture GVA grew slightly faster than the UK economy (25.4% vs 24.3%).

DCMS said the increase in cultural sector GVA was almost entirely due to a 4.1% increase in the ‘film, TV and music’ subsector.

The subsectors that saw the largest relative growth in cultural sector GVA were the ‘radio’ which increased by an estimated 11.8% and ‘crafts’ subsector which grew by an estimated 4.9%.

‘Film, TV and music’ is the largest cultural subsector in size economically, contributing an estimated £23.8bn to the UK economy in 2024. The second largest is ‘arts’ with £11.4bn.

Growth in cultural sector subsectors, in chained volume measures (CVM):

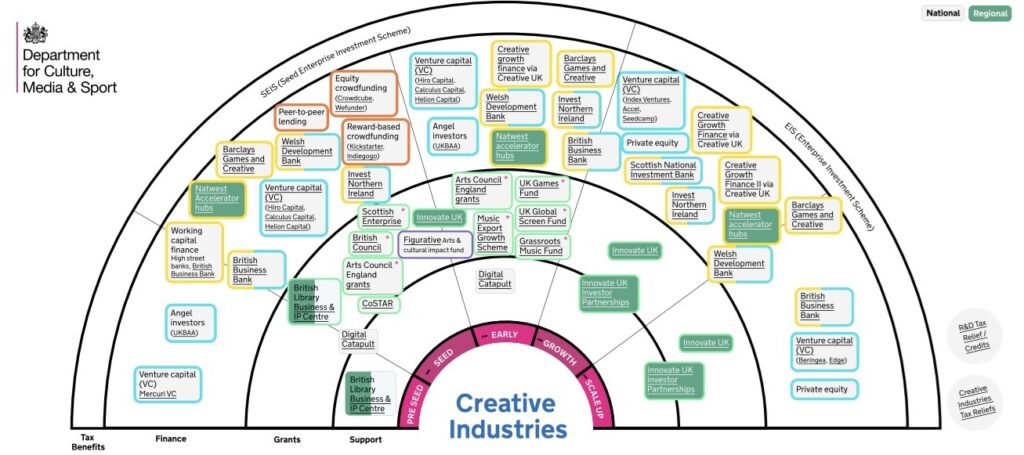

Alongside the data for the growth of the creative industries, the government has announced new funding and related support for creative businesses.

It follows the publication last year of the creative industries sector plan. In addition, the creative industries is one of the eight key sectors of focus in the government’s industrial strategy and the West of England is one of the government’s priority areas for the creative industries. As part of that, the £25m Creative Places Growth Fund will run for three years from April 2026.

The new funding and support announced this month is:

DCMS has also published new resources to help creative businesses access funding including a map of finance available to the sector, and case studies of successful creative scale-ups.

Bristol Creative Industries also a regularly updated guide to funding for creative industries businesses in the West of England here.

Click on the map for links to all the sources of creative industries funding

In summer 2021 we ran an event discussing funding for creative businesses with the south west team at Innovate UK EDGE and a group of Bristol Creative Industries members.

During the discussion, attendees said it would be useful if we could provide regular updates on the finance schemes that are available for creative companies in the south west and beyond. This guide is our response.

The guide is one of Bristol Creative Industries’ most popular ever blog posts. We keep it updated with the latest funding schemes for creative businesses so check it regularly. We also include the post in our monthy email newsletter, BCI Bulletin. To sign up, go here.

Funding news:

The West of England is one of the government’s priority areas for the creative industries and the West of England Combined Mayoral Authority will receive £25m of the funding to support the region’s creative industries through the Creative Places Growth Fund.

The funding will run for three years from April 2026. Read more details about the fund here.

The British Business Bank, the government-owned business development bank, has launched the £200m South West Investment Fund (SWIF) “to help address market failures by increasing the supply and diversity of early-stage finance for UK smaller businesses, providing funds to firms that might otherwise not receive investment”.

Aimed at businesses in Bristol, Cornwall and the Isles of Scilly, Devon, Dorset, Gloucestershire, Somerset and Wiltshire, the fund provides:

SWIF is managed by four fund managers:

The region is split as follows:

North of the region:

South of the region:

The funding is split as follows:

Businesses can apply for funding directly to the relevant fund managers here.

Grants of £2,500 to £10,000 are available to help small businesses, sole traders, charities, community interest companies (CICs), community organisations and creative and cultural groups open new premises.

The deadline for applications is 11.59pm on Monday 30 November 2026.. If all available funding is allocated before the deadline, the scheme may close early.

Successful applicants must start trading from the funded property by Friday 26 February 2027.

This £35m Creative UK and Triodos Bank investment fund provides loans of £100,000 to £1m.

Finance is directed to post-revenue creative businesses presenting promising growth potential and who:

PRS Foundation offers various grant funding schemes for music creators and organisations, including The Open Fund for Music Creators and The PPL Momentum Music Fund for artists/bands to break through to the next level of their careers.

The Black Artists Grant, offered by Creative Debuts, is £500 no-strings attached financial support to help Black artists.

The fund is an open access programme for arts, libraries and museums projects.

Funding of between £1,000 and £100,000 is available.

Loans of between £100,000 and £1.5m to UK charities and social enterprises based in England, Wales and Scotland.

Established games companies with a track record and a game development project at an early stage can apply for grants up to £100,000.

The deadline is 12pm on 5 May.

Grants of £100,000 – £250,000 for games companies with a commercial entertainment game prototype.

Funding of between £20,000 and £50,000 for social enterprises grow. Repayments are based on a percentage of revenue so if revenue falls, repayments reduce.

This fund from Arts Council England supports individual cultural and creative practitioners in England thinking of taking their practice to the next stage through things such as: research, time to create new work, travel, training, developing ideas, networking or mentoring.

Grants of between £2,000 and £12,000 are available.

The next round of funding will open to applications in June 2026.

The £5m Supporting Grassroots Music fund supports rehearsal and recording studios, promoters, festivals, and venues for live and electronic music performance.

Craft practitioners and organisations can apply for small grants to fund projects that support endangered crafts. The deadline is 5pm on 8 May.

Travelwest provides match-funded grants for initiatives that improve sustainable travel provision in a business.

The aim is to provide financial support and incentives to employers to enable them to encourage sustainable modes of commuting or in-work travel (including site visits and meetings) amongst their staff.

The grants can be used for the implementation of physical measures, promotional events or any other measure that will encourage mode change amongst staff.

Grants are currently availables for businesses in Bristol and North Somerset.

Innovate UK’s £100m BridgeAI programme aims “to help businesses in high growth potential sectors such as creative industries, agriculture, construction, and transport to harness the power of AI and unlock their full potential”.

The programme offers funding and support to help innovators assess and implement trusted AI solutions, connect with AI experts, and elevate their AI leadership skills.

This fund supports organisations who work at the intersection of art and social change. It offers grants between £90,000 and £300,000 over three years.

Applications are currently closed but details of the next round will be announced soon.

This new £23m social impact investment fund is for socially driven arts, culture and heritage organisations registered and operating in the UK. It offers loans between £150,000 and £1m repayable until May 2030.

The Elephant Trust says its mission is to “make it possible for artists and those presenting their work to undertake and complete projects when frustrated by lack of funds. It is committed to helping artists and art institutions/galleries that depart from the routine and signal new, distinct and imaginative sets of possibilities.”

Grants of up to £5,000 are available. The next round of funding is expected to open soon.

Grants of up to £100,000 are available for arts, libraries and museums projects.

The grants support a broad range of creative and cultural projects that benefit people living in England. Projects can range from directly creating and delivering creative and cultural activity to projects which have a longer term positive impact, such as organisational development, research and development, and sector support and development.

The UK Global Screen Fund (UKGSF) is designed to boost international development, production, distribution, and promotional opportunities for the UK’s independent screen sector. It has the following schemes:

This fund aims to grow exports and global demand for UK independent film by supporting the UK film industry to achieve measurable results which would not have been achievable without the support.

Applications close on at 11.59pm on 31 March 2028.

This scheme supports the festival launch of UK films in order to enhance their promotion, reach and value internationally.

Applications close on at 11.59pm on 31 March 2028.

Supports UK producers to work as partners on international co-productions and help create new global projects.

The next round of funding is due to open for applications in September 2026.

Awarding National Lottery funding to develop innovative new solutions which tackle the UK screen sector’s most critical challenges.

Between 2026 and 2029, up to 12 challenge calls will be identified where innovative new thinking could catalyse a step change in the industry, while producing learning and insights that benefit the whole screen sector.

Up to £150,000 is available for immersive works of fiction from experienced UK producers and creative leads with a track record in immersive or related screen-based practice.

The deadline is 12pm on 3 June 2026.

Funding for factual immersive screen projects.

Supports early career filmmakers with original and fictional shortform projects of up to 15 minutes in length in live action, animation and immersive/virtual reality.

Grants awards of between £5,000 and £25,000 are available. The next round of applications is scheduled for spring 2027.

Thsis scheme awards National Lottery funding to support the exhibition and distribution of nationally significant audience-facing independent film and immersive projects.

A Start Up Loan is a government-backed unsecured personal loan for individuals looking to start or grow a business in the UK. Successful applicants also receive 12 months of free mentoring and exclusive business offers.

All owners or partners in a business can individually apply for up to £25,000 each, with a maximum of £100,000 per business.

The loans have a fixed interest rate of 6% p.a. and a one to five year repayment term. Entrepreneurs starting a business or running one that has been trading for up to three years can apply. Businesses trading for between three and five years can apply for a second loan.

If you’re running a creative social enterprise you may be able to access funding from UnLtd.

Finance of up to £5,000 is available for starting a social enterprise and up to £15,000 for growing a social enterprise.

Successful applicants also get up to 12 tailored business support plus access to access to expert mentors and workshops.

Businesses can apply for up to £3,500 to cover the costs of installing gigabit broadband.

Check if the scheme is available in your area here.

Grants to provide support towards the costs of the purchase, installation and infrastructure of electric vehicle chargepoints at eligible places of work.

The scheme covers up to 75% of the total costs of the purchase and installation of EV chargepoints (including VAT), capped at a maximum of £350 per socket and 40 sockets across all sites per applicant.

The deadline for applications is 11.59pm on 31 March 2027.

This grant supports the uptake of electric vans and trucks. It currently offers discounts up to £2,500 for small vans, £5,000 for large vans, £16,000 for small trucks, and £25,000 for large trucks.

On 18 August 2025 the government announced the plug-in van and truck grant has been extended until 2027.

If you know of another scheme that we haven’t listed and you’d like to share it with other creative businesses, email Dan to let us know.

Web developers, digital innovators and tech professionals are gearing up for the sixth annual Umbraco Spark innovation conference, returning to Bristol this spring at We The Curious on Friday 20 March 2026. Organised by Bristol digital agency Gibe Digital, the event has become a fixture for developers from across the UK and Europe to share insights, ideas and practical knowledge around the open‑source Umbraco CMS and broader .NET ecosystem

Speaking about the conference, Steve Temple, Technical Director and Co‑founder of Gibe Digital, describes Spark as “a calendar highlight” that brings together “so many talented developers from the amazing Umbraco community.” Steve adds that the event leaves attendees “feeling inspired, armed with fresh knowledge to take your Umbraco projects to the next level.”

This year’s programme features a single main track of deep‑dive technical talks, practical demos and forward‑thinking sessions on topics such as load‑balancing for scalable apps, Umbraco Search, next‑generation back‑office features, and experimenting with AI‑driven accessibility tools.

Schedule Highlights:

Thursday, 19 March – The day before the main conference kicks off with a full-day Hackathon & Package Jam for the community, followed by a pre-party at a local game bar with ping pong, bowling, karaoke, food and drinks.

Friday, 20 March – A Harbour Run at 7 AM starts the day, followed by registration with coffee and pastries. The main track runs 9 AM–5:30PM, featuring technical talks, lightning sessions and demos. The Package Awards celebrate standout contributions, and the day wraps up with an after-party. Attendees also benefit from lunch, refreshments, a free cloakroom, and quiet/multi-faith rooms to support wellbeing.

Tickets & Pricing: Standard tickets cost £150 + VAT, available until the end of February or until sold out. Grab your ticket here.

Umbraco Spark continues to cement Bristol’s status as a hub for creative tech events — combining local community energy with the global expertise of the Umbraco ecosystem.

Omni Productions has been appointed by AXA to develop a global, video-led workplace training programme to help organisations better support employees affected by domestic and sexual violence.

Built around drama-led films and expert interviews, Safe Spaces translates complex subject matter into accessible training for employees across multiple markets. Omni led the creative development from research and scripting through to production, shaping the narratives to be engaging, human-centred, and effective for global workplace training.

The programme builds on AXA’s long-standing ‘We Care’ initiative and its commitment to employee protection. Domestic and sexual violence affects millions of people each year, with the workplace often serving as a safe space outside the home. In England and Wales alone, an estimated 2.3 million people experience domestic violence and abuse annually, placing employers in a unique position to recognise warning signs and offer support.

The campaign is built around the Recognise, Respond, Refer (3R) framework, which underpins the films and learning content. Rather than focusing on awareness alone, the programme demonstrates what action looks like in real workplace situations to help employees recognise signs of abuse, respond appropriately and direct people to specialist support.

Omni’s role was to translate that ambition into a campaign that people would engage with. Working closely with AXA’s HR, inclusion and communications teams as a strategic partner, Omni’s brief was to turn a highly sensitive topic into training that is human, practical and ethically produced.

Video and drama-led storytelling was chosen to engage audiences emotionally, helping them understand lived experiences without sensationalism.

All stories, scripts, drama scenarios and supporting interviews were developed through an expert-led process. Omni worked alongside domestic abuse experts, NGOs and survivor-support organisations to ensure accuracy, cultural sensitivity and relevance to workplace contexts.

Sam Hearn, co-founder and managing director at Omni, said: “This type of work sits at the heart of what we do. Safe Spaces shows the power of human storytelling when addressing complex subjects such as domestic and sexual violence. Drama allows people to understand context and connect emotionally, which is essential for a subject like this. Each film was shaped in close collaboration with people with lived experience and sector specialists, whose insights were essential to keep the stories authentic.

As an agency, we aim to create work that truly matters, and our B Corp values guide how we approach sensitive topics to ensure they are both responsible and impactful. Partnering with AXA, we set out to create training that could genuinely change how people recognise and respond to abuse in the workplace.”

Safe Spaces is rolling out globally in phases, with content currently available in 11 languages and further versions in development. The assets integrate into local learning systems, allowing pledged organisations to deliver the training in ways that suit their workforce.

Early engagement on the Safe Spaces platform shows a strong impact, with high numbers of returning visitors. Safe Spaces has already been adopted by organisations beyond AXA, with further companies confirming participation, including L’Oreal, Accor, Engie, LVMH, Orange and Publicis France.

Kirsty Leivers, chief culture, inclusion and diversity officer at AXA, said: “Working with Omni on Safe Spaces has been a collaborative and creative process. From the outset, the team demonstrated a deep understanding of the sensitivity and importance of this subject, approaching every stage with empathy and creativity. The result is a powerful and accessible platform that supports our shared commitment to building more supportive workplaces.”

The project also highlights that human storytelling remains critical in an AI-first era. While automation is reshaping content production, Safe Spaces demonstrates how drama-led video allows employees to connect with real experiences to build empathy and the confidence to act.

Hearn added: “Although AI is changing how content is made, sensitive issues still need human insight and care. Safe Spaces shows how video can make complex topics tangible and actionable, even at a global scale.”

The programme is designed to evolve, with AXA and Omni exploring further developments across 2026, ensuring the training continues to deliver measurable impact across global workplaces.

Last week, the Gather Round at Brunswick Square was buzzing. A packed room, a hum of anticipation, and a palpable sense that something meaningful was about to unfold as we kicked off the third year of our award-winning series, Gather Round Presents.

From the very first moment, the evening invited us into stories that stretched beyond words on a page. Our panellists didn’t just tell stories: they cracked them open. Stories of human understanding, our relationship with the world around us, and the narratives we carry about ourselves and others. Together, they explored how the past can be re-examined, reshaped, and used to imagine new futures and how powerful it feels when those stories land.

Sara Joyner, Senior Podcast Producer, opened the evening and wasted no time pulling us in. What began with a slightly shocking story instantly had the room leaning forward, unsure where it might lead. But that uncertainty quickly turned into delight as Sara revealed her craft with warmth, humour, and total ease.

With sticky notes representing three characters in an upcoming podcast, Sara physically rearranged the facts in front of us, showing, in real time, how a story can be subtly shaped. Laughter rippled through the audience as she explained, with playful honesty, how she “manipulates” the listener.

As the audience was invited to guess where the story was heading, there was a collective realisation: context is everything. By withholding or revealing certain details, a story and a person can be perceived in entirely different ways. Sara’s delivery was disarming and deeply engaging, leaving us entertained, slightly unsettled, and newly aware of how easily we’re led… often without noticing.

Connect with Sara on LinkedIn or check out her web page for more info on her work.

Dan Caulfield, Film Director and Storyteller at Enviral, followed and had us hooked within seconds. He began with what felt like a deeply emotional story: a grieving father, a lost child, and an epic journey born of love and loss. The room softened.

And then, laughter erupted.

The characters were revealed to be Marlin and Nemo. Pixar, of course. A collective groan, smile, and appreciation washed across the room.

He wasn’t done yet. The second story, a tender, hilarious retelling of a tale once told to him by his Irish grandad in a pub, had us in stitches. Dan described piecing together meaning from thick accents, facial expressions, and half-heard words, transporting us back to a time when storytelling was something you felt as much as heard.

Behind the humour was something deeper. Dan spoke passionately about the ancient tradition of oral storytelling and the responsibility of keeping it alive. Though he works in marketing, this wasn’t a sales pitch. It was human.

Stories, he reminded us, exist everywhere across cultures, languages, and generations. They shape who we believe we are. They can fuel fear… or they can bring us together. As the laughter settled, the room grew reflective. Dan invited us to consider the stories we tell ourselves about identity, worth, and belonging. Food for thought that lingered long after he left the stage.

Follow Dan on Instagram or connect with him on LinkedIn to see more of his work.

Ghostwriter and part-time stand-up comedian Nick Anderson Vines carried us into the first break and promptly had the room roaring. Sharp, self-aware, and genuinely funny, Nick brought a different energy while still keeping storytelling firmly at the centre.

He spoke about how he works LinkedIn with refreshing honesty, unpacking how to attract clients while still telling meaningful stories. When ChatGPT entered the scene in 2023, Nick admitted it shook the writing world fear, uncertainty, and the sense that everything might change overnight.

But then came the shift. Opportunity. A return to craft. Writing more. Writing better.

Nick’s passion was contagious. In a fast-moving digital landscape, he argued, stories are what stops the scroll. They’re what make us care. Using the pull of before and after, and reframing narratives with intention, Nick left us laughing — and quietly fired up to rethink how we tell stories online.

Connect with Nick on LinkedIn to hear more about his work.

Rosa ter Kuile, known as RTiiiKA, gently reset the room as the only visual artist on the panel. Her presence felt grounding, inviting us to slow down and see stories differently.

Rosa spoke about storytelling beyond words: through murals, characters, and playful alter egos. From the giant foyer mural at Bristol Beacon to the personas she created and played in videos to tell her story – ‘Grinder Guy’ and her ‘own agent’. She showed how storytelling can be both strategic and deeply personal and sometimes with a touch of humour. These characters, she explained, often became the most compelling part of her work — a way to narrate process, vulnerability, and creativity in real time.

As Rosa shared the recurring themes that shape her art: sexuality, falling in love, road signs, bikes (and more) the message became clear: stories exist everywhere. Some shout. Others whisper. It’s up to us to notice them.

Follow Rosa on Instagram to see more of her creations or connect with her on LinkedIn.

Mark DeLisser stepped onto the stage and immediately stilled the room opening with a poem from his new book, Ashes to the Breeze.

Mark spoke about his deep relationship with the natural world, and the idea that while he writes stories, often as poems, he is also being storied. By landscapes. By relationships. By life itself. There was a quiet reverence in his words as he described knowing he is part of something far bigger, a story that began before him and will continue long after.

He spoke of listening to the body while writing, noticing moments of tightening, softening, longing — and allowing those sensations to guide the words. Poetry, he said, comes from slowing down and noticing, not forcing meaning into existence.

Sharing two poems: Your Name and The Stories We Tell. Mark echoed something Dan had said earlier: the importance of telling stories about what we want to be true. Stories that interrupt the constant stream of horror and remind us of other ways of living. In that moment, it felt like the room was breathing together inspired, hopeful, and deeply moved.

You can buy Mark’s book Ashes to the breeze in Waterstones.

And follow him on Instagram to hear more of his beautiful words.

With just 24 hours’ notice, Kendra Futcher OG Cigar Factory member closed the evening, and what a closing it was. Ever-eloquent, deeply present, and emotionally generous, Kendra held the room with quiet power.

A self-described writer, thinker, and noticer, she spoke about paying attention to the smallest details: the inflection of a voice, a texture, a sound, the scrunch of a nose. This practice of noticing, she shared, became vital during Covid a way to stay alive to the world and to herself.

Kendra spoke about vulnerability as the beating heart of storytelling. Emotional honesty, she reminded us, is what truly connects people. Words can divide but they can also unite.

She spoke of her collection of photographs from protests placards filled with raw, urgent language that has so inspired her. She shared two poems with us – the first, Monobrow, about her daughter, silenced the room completely. It was her first time reading the poem aloud, and the moment felt sacred. You could feel the tears, the tenderness, the shared humanity.

For Kendra, truth is freedom. And that, she believes, is the essence of storytelling.

Follow Kendra on Instagram or connect with her on LinkedIn or have a look at her website to read more about her many skills.

Our beautiful event space at Brunswick Square is available for hire, email Hannah on [email protected] for more info and come and host your event at our place!

Follow us on Instagram for more stories from our creative community and if you want to come and join us, we’re currently offering 30% off for 3 x months if you join before 28th February 2026,more info on our offer page.

You need to load content from reCAPTCHA to submit the form. Please note that doing so will share data with third-party providers.

More Information